Introduction

Regulators aren't waiting for fintechs and payments companies to catch up. TD Bank's $3.1 billion penalty in 2024 for systemic transaction monitoring failures and Block's $40 million fine in 2025 for inadequate customer due diligence are sharp reminders: FinCEN, the BSA, and FATF apply pressure regardless of company size.

The cost of compliance is real. The cost of non-compliance is often catastrophic.

Most organizations still underestimate what building an in-house AML program actually costs. Personnel overhead, technology investments, and ongoing program maintenance routinely exceed initial projections — leading more financial services leaders to ask: is outsourcing the smarter path forward?

Key Takeaways

- AML compliance costs fall across three pillars: people, processes, and technology

- A fully staffed in-house AML program can cost hundreds of thousands of dollars annually

- Non-compliance carries steep penalties—FinCEN issued a record $1.3 billion fine to TD Bank in 2024

- Outsourcing consolidates costs and delivers CAMS-certified expertise, scalable capacity, and audit-ready programs

- A strong partner provides end-to-end support with U.S. regulatory experience and risk-tailored solutions

Breaking Down the True Cost of AML Compliance

The actual cost of AML compliance extends far beyond software subscriptions. Organizations must account for three interconnected cost pillars: people, processes, and technology. Underestimating any one of these leads to budget overruns and compliance gaps.

People

A functional AML program requires specialized personnel. At minimum, you need an AML analyst for transaction monitoring and investigations, plus a compliance officer or director for oversight and regulatory accountability. These roles demand specific qualifications — CAMS certification, BSA/FATF regulatory experience, and a background in financial crime risk management.

U.S. salary benchmarks reveal the true cost:

- AML Analyst: Median salary of $88,637, with the 75th percentile reaching $117,462

- Compliance Officer: Median salary of $119,977, with the 75th percentile at $162,980

- AML Director: Median salary of $227,789, with top earners exceeding $294,461

These figures represent base compensation only. Total employment cost adds benefits, payroll taxes, training, and ongoing professional development—easily adding 25-40% to each salary figure.

Processes

AML compliance isn't a set-it-and-forget-it operation. It's a continuous, high-effort obligation requiring dedicated resources year-round. Core process requirements include:

- Customer Identification Program (CIP): Risk-based procedures to verify customer identity

- Customer Due Diligence (CDD/EDD): Identifying and verifying beneficial owners, conducting enhanced due diligence for high-risk customers

- Ongoing KYC monitoring: Continuous review of customer activity and profile updates

- Transaction monitoring: Real-time and batch analysis to detect suspicious patterns

- SAR/UAR filing: Investigating and reporting suspicious activity within regulatory deadlines (30 days from initial detection)

- Annual risk assessments: Evaluating enterprise-wide money laundering and terrorist financing risks

- Program development and refresh: Updating policies and procedures to reflect regulatory changes

- Independent testing: Periodic audits of the BSA/AML program by internal or external parties

None of this can be absorbed by a part-time employee or handed off to a CFO without compliance experience — these obligations require dedicated, qualified personnel who understand financial crime risk from the ground up.

Technology

Building a compliant AML technology stack requires multiple integrated systems:

- KYC/sanctions/PEP screening software for customer onboarding and ongoing monitoring

- Customer identification tools for document verification and biometric authentication

- Electronic customer file systems with risk rating capabilities

- Transaction monitoring software to detect suspicious patterns and generate alerts

According to industry benchmarks, the combined annual cost of these technologies easily exceeds $100,000 for small-to-medium entities. Variable API-based pricing adds complexity—identity verification can cost $0.10 to $1.50 per check, biometric liveness checks range from $0.25 to $2.00 per session, and AML screening runs $0.05 to $0.80 per search.

Technology costs don't remain static, either. Systems must evolve continuously to combat new money laundering typologies, accommodate business growth, and reflect regulatory changes — making this a recurring, escalating line item that grows alongside your program.

The Cost of Getting It Wrong

Failing to maintain an adequate AML program carries financial consequences that often dwarf the cost of compliance itself. Recent enforcement actions illustrate the magnitude of regulatory penalties:

| Institution | Year | Penalty | Violation |

|---|---|---|---|

| TD Bank | 2024 | $3.1 billion | Systemic transaction monitoring failures; intentionally excluded domestic transactions from monitoring |

| Binance | 2023 | $4.3 billion | Willful failure to implement effective AML program; failure to register as MSB |

| OKX | 2025 | $504 million | Operated unlicensed money transmitting business; knowingly violated AML laws |

| Block (Cash App) | 2025 | $40 million | Inadequate customer due diligence; severe transaction alert backlog |

The dollar figures are striking, but monetary penalties are only part of the exposure. Inadequate AML programs trigger non-financial consequences that can be existential for fintechs and payments companies:

- Reputational damage that erodes customer trust and brand value

- Loss of banking partnerships or payment processing relationships

- Heightened regulatory scrutiny including consent orders and enhanced supervision

- Criminal prosecution of executives under the Bank Secrecy Act

For fintechs relying on sponsor banks or correspondent banking relationships, losing a banking partner can mean the end of operations. The Bank Secrecy Act of 1970 carries both civil and criminal penalties. Willful violations can result in fines up to $500,000 and 10 years in prison when part of a pattern of illegal activity.

In-House vs. Outsourced AML: A Practical Comparison

Choosing between in-house and outsourced AML compliance requires understanding one critical fact: outsourcing does not transfer legal liability. The 2023 Interagency Guidance on Third-Party Relationships explicitly states that financial institutions remain responsible for meeting AML obligations to the same extent as if activities were performed in-house. Responsibility stays with the institution, regardless of who performs the work.

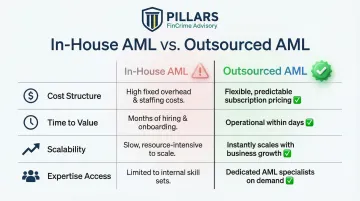

Key decision factors:

| Factor | In-House | Outsourced |

|---|---|---|

| Cost Structure | High upfront investment in salaries, benefits, training, and technology; fixed costs regardless of volume | Predictable service fees that scale with activity; people, process, and technology bundled into one engagement |

| Time to Value | Months to recruit, onboard, and train qualified staff before program components are operational | Faster deployment using pre-built frameworks and experienced professionals |

| Scalability | Hiring and training lag behind transaction volume growth | Provider adjusts service levels without recruitment delays |

| Expertise Access | Dependent on internal talent acquisition; limited exposure beyond your organization | Access to CAMS-certified professionals with experience across multiple institutions and risk profiles |

These tradeoffs point clearly toward different paths depending on your organization's size, stage, and resources.

Which organizations should build in-house?

Large, established institutions with:

- Significant compliance budgets and infrastructure

- Complex, highly customized requirements

- Regulatory expectation of dedicated internal teams

- Sufficient transaction volume to justify full-time specialized staff

Which organizations are better served by outsourcing?

- Fintechs and growth-stage payments companies

- Institutions with limited compliance headcount

- Organizations new to AML obligations

- Companies facing rapid scaling challenges

- Firms preparing for regulatory exams without internal expertise

Addressing the control concern:

Outsourcing requires trusting a third party with sensitive compliance processes and customer data. Mitigate this through written service agreements that define scope, performance expectations, escalation procedures, and data security standards.

Maintain internal oversight through regular performance reviews and documented monitoring of outsourced work. Regulators expect active supervision of third-party relationships — not passive delegation.

Why Outsourcing Is a Smart Move for Fintechs and Financial Institutions

Cost Efficiency

Outsourcing consolidates the three cost pillars—people, process, and technology—into a single service engagement. You eliminate the need to:

- Recruit and retain CAMS-certified staff at competitive salaries

- Purchase and maintain multiple software platforms

- Build compliance infrastructure from scratch

- Absorb benefits, training, and turnover costs

This consolidated model converts unpredictable fixed costs into predictable variable costs that scale with your business.

Specialized Expertise

Reputable AML outsourcing partners bring financial crime knowledge that's difficult and expensive to replicate internally. They offer:

- Regulatory awareness across FinCEN, FATF, and banking agency requirements

- Experience implementing programs across multiple institutions and risk profiles

- Exposure to emerging money laundering typologies and detection techniques

- Established relationships with regulatory bodies

This breadth of experience is valuable for organizations new to compliance or entering new regulatory jurisdictions.

Scalability for Growth

Fintechs and payments companies often experience rapid, unpredictable growth. Transaction volumes can double in months, new products launch with different risk profiles, and geographic expansion introduces new regulatory requirements. Your AML program must scale in parallel.

A qualified outsourcing partner adjusts service levels to match growth without the lag of hiring and onboarding new compliance staff. When you launch a product requiring enhanced due diligence or enter a new market, the provider adapts immediately.

Audit Readiness

A well-structured outsourcing engagement delivers a program that is documented, tested, and demonstrably compliant. This reduces stress around regulatory exams and internal audits.

Firms like Pillars FinCrime Advisory provide full lifecycle support—from policy development and risk assessments through transaction monitoring optimization and audit readiness. The result: stronger alert quality, lower operational friction, and a program that holds up when examiners come knocking.

How to Choose the Right AML Outsourcing Partner

Not every AML outsourcing provider is built for your business. Evaluate prospective partners across five criteria before signing anything:

CAMS Certification and Regulatory Experience

- Verify that professionals are CAMS-certified with hands-on U.S. regulatory experience

- Confirm familiarity with BSA requirements, FinCEN rules, and FATF guidelines

- Review track record supporting organizations similar to yours in size, industry, and risk profile

Tailored, Not Template-Based Programs

Generic AML programs create compliance gaps — they're built for no one in particular. Your partner must:

- Conduct thorough risk assessments specific to your business model

- Design policies and procedures that reflect your actual operations

- Customize transaction monitoring scenarios to your transaction types and customer base

- Understand your jurisdiction's specific regulatory requirements

Comprehensive Service Scope

Evaluate whether the provider covers the full program lifecycle:

- Policy and procedure development

- Risk assessment and program design

- Transaction monitoring optimization

- KYC/KYB process design and implementation

- SAR investigation and filing support

- Regulatory exam preparation and audit readiness

- Ongoing program maintenance and updates

Written Agreements and Oversight Framework

Establish a written outsourcing agreement that defines:

- Scope of services and deliverables

- Performance expectations and service level agreements

- Escalation procedures for suspicious activity and regulatory inquiries

- Data security standards and breach notification protocols

- How you will monitor and review the outsourcing arrangement

Maintaining internal oversight is non-negotiable — you can delegate tasks, but regulatory responsibility stays with your organization.

Practical, Data-Driven Approach

The right partner improves program performance — not just documentation. They should:

- Focus on outcomes, not just checkbox compliance

- Use data to optimize transaction monitoring and reduce false positives

- Provide transparent reporting on program performance

- Adapt quickly to regulatory changes and emerging risks

Frequently Asked Questions

What is AML/CFT outsourcing?

AML/CFT outsourcing means contracting a specialized third party to perform anti-money laundering and counter-terrorism financing compliance functions on your behalf. Your organization retains full legal responsibility for meeting regulatory obligations, while the provider delivers the expertise, processes, and technology to execute the program.

What are the AML compliance requirements?

Core U.S. AML requirements under the Bank Secrecy Act include:

- Customer Identification Programs (CIP) and Customer Due Diligence (CDD), including beneficial ownership verification

- Transaction monitoring to detect and report suspicious activity

- Suspicious Activity Report (SAR) filing within regulatory deadlines

- Ongoing enterprise-wide risk assessments

Can internal audit be outsourced?

Yes, independent testing and internal audit functions within an AML program can be outsourced—this is common practice. However, your organization must maintain oversight and cannot abdicate responsibility for audit findings or remediation of identified deficiencies.

What is the landmark law targeting money laundering?

The Bank Secrecy Act (BSA) of 1970 is the foundational U.S. anti-money laundering law, requiring financial institutions to assist government agencies through recordkeeping and reporting. It has since been expanded by the USA PATRIOT Act (2001) and the Anti-Money Laundering Act of 2020.

What are the four types of outsourcing?

The four general outsourcing types are:

- Professional/knowledge process outsourcing — specialized expertise such as legal or compliance

- IT outsourcing — technology infrastructure and support

- Business process outsourcing — routine operational tasks like payroll

- Managed services outsourcing — ongoing operational responsibility for specific functions

AML compliance outsourcing typically falls under professional/knowledge process or managed services outsourcing.

Pillars FinCrime Advisory provides end-to-end financial crime compliance support for fintechs, payments companies, and financial institutions. From policy development and risk assessments to transaction monitoring optimization and regulatory exam readiness, our CAMS-certified team builds programs that are audit-ready and built to scale.

Contact us today:

- Phone: 281-825-1603

- Email: pillarsfincrimeadvisory@gmail.com

- Location: Houston, Texas (serving clients nationwide)