Introduction

Fintechs face a unique operating challenge: they must scale fast while regulatory requirements shift beneath them. Hiring specialized talent is slow and expensive. For many fast-growing companies, outsourcing has become a strategic response—not just a cost-cutting move.

Fintech outsourcing spans a wide range of functions—software development and customer support, but also financial crime compliance, data analytics, and back-office operations. Which functions you outsource, and to whom, has real consequences for how your company scales and how it holds up under regulatory scrutiny.

This article walks through the most commonly outsourced services in fintech, what makes each one distinct, and how to decide what belongs outside your walls.

TLDR

- Fintech outsourcing covers technology, operations, compliance, and advisory functions—not just software development

- Financial crime compliance (AML, KYC, transaction monitoring) is one of the most high-stakes services fintechs outsource and one of the most commonly mishandled

- The right outsourcing decision depends on the function's complexity, regulatory exposure, and whether it requires specialized expertise your team doesn't have

- Outsourcing works best when scope, accountability, and compliance expectations are defined before a partner is engaged

What Is Outsourcing in Fintech and Why Does It Matter?

Fintech outsourcing means engaging a third-party provider to handle a specific business function or set of tasks that would otherwise be managed internally. This ranges from technology builds to operational and compliance work.

Outsourcing has accelerated in fintech because these companies operate in a high-growth, heavily regulated environment. Hiring specialized talent in-house is slow and expensive, and regulatory requirements demand expertise that evolves constantly.

That said, the 2023 US Interagency Guidance on Third-Party Relationships is clear: regulated financial institutions must maintain ultimate accountability for third-party functions. Outsourcing compliance or operations does not remove your regulatory obligations.

Most fintechs use a hybrid model rather than a binary in-or-out approach. Core IP and strategy stay in-house, while execution capacity extends externally for functions that are:

- Specialized (AML/BSA, KYC, fraud risk)

- High-volume (transaction monitoring, customer onboarding)

- Compliance-sensitive (regulatory exam readiness, policy development)

Common Outsourced Services in Fintech

Fintech outsourcing covers five broad functional areas. Each serves a different operational need and carries different risk and compliance considerations.

Software Development and IT Services

This is the most widely recognized outsourced service. It includes building or maintaining financial software, mobile apps, payment platforms, and integrations with external systems like banking APIs or data providers.

Who benefits most:

- Early-stage fintechs validating MVPs

- Growth-stage companies running parallel product lines without disrupting live systems

- Organizations seeking speed-to-market advantage and access to specialized technology talent

Limitation to watch: Software outsourcing in fintech requires partners who understand regulatory constraints such as PCI DSS and GDPR. Generic software firms without fintech experience often create security and compliance gaps that surface during audits.

Customer Support and Contact Center Services

This involves outsourcing the entire customer-facing support function to a dedicated third-party team. It includes live chat, phone support, dispute resolution, and onboarding assistance—often across multiple channels and time zones.

Strengths:

- 24/7 availability

- Scalability during high-volume periods

- Frees internal teams from repetitive queries to focus on complex issues or product development

Trade-off: In fintech, customer support teams handle sensitive financial data and complaints that can have regulatory implications. Partners must be trained in compliance protocols, data handling standards, and escalation procedures.

Back-Office Operations and Administrative Functions

Typical functions outsourced here include:

- Accounting and payroll processing

- Accounts receivable and payable

- Data entry and document processing

- Loan or payment operations support

Fintechs outsource these because they're high-volume and process-driven. Delegating them reduces overhead and operational friction while improving accuracy.

Data Analytics and Business Intelligence

Outsourced analytics engages external specialists to manage large data sets, build predictive models, and generate the risk and business intelligence insights that drive product and compliance decisions.

Common use cases include:

- Customer behavior analysis and segmentation

- Fraud pattern detection and risk scoring

- Regulatory reporting and compliance dashboards

- Predictive modeling for credit or transaction risk

Cybersecurity

Cybersecurity outsourcing provides continuous protection through security monitoring, penetration testing, and vulnerability management. It gives fintechs access to specialized expertise and audit-ready documentation without building an internal Security Operations Center.

According to FFIEC BSA/AML guidance, financial institutions must implement appropriate controls and monitoring — especially when working with third-party payment processors.

Marketing, HR, and Strategic Advisory

Outsourced marketing covers content, SEO, digital campaigns, and lead generation. HR/talent acquisition outsourcing helps fintechs grow teams without building permanent internal departments for non-core activities. These functions allow fintechs to maintain brand presence and recruiting momentum while focusing internal resources on product and compliance.

Financial Crime and Compliance Outsourcing: Why Fintechs Get This Wrong

Financial crime compliance deserves a separate, deeper discussion. AML/BSA programs, KYC/CDD processes, transaction monitoring, SAR filings, and audit readiness are not just operational functions. They are regulatory obligations with direct consequences for licensing, examinations, and reputational standing.

What Compliance Outsourcing Covers When Done Well

Fintech compliance outsourcing should include:

- Policy development and program design

- BSA/AML risk assessments

- Transaction monitoring tuning and alert optimization

- Customer due diligence workflows

- Sanctions screening

- Preparation for regulatory exams or third-party audits

According to FinCEN's 2024 proposed AML/CFT program requirements, "the duty to establish, maintain, and enforce a financial institution's AML/CFT program shall remain the responsibility of, and be performed by, persons in the United States who are accessible to, and subject to oversight and supervision by, the Secretary and the appropriate Federal functional regulator." You can outsource execution, but you cannot outsource accountability.

What Goes Wrong When Fintechs Underinvest

Compliance programs built without domain expertise generate excessive false positives, miss real risk signals, fail examinations, and create regulatory liability. This is a common failure point for fast-growing fintechs that prioritize product over compliance infrastructure.

The root of that failure is often a category error — fintechs conflate compliance technology with compliance expertise:

- Regtech and cybersecurity tools automate screening, flag transactions, and generate alerts

- Financial crime program management requires human judgment to design the program, tune the tools, interpret the results, and defend decisions to examiners

Many fintechs end up well-tooled but under-guided. A regtech platform does not replace a CAMS-certified compliance professional who understands BSA/AML program design and regulatory expectations.

That gap — software without qualified oversight — is exactly what firms like Pillars FinCrime Advisory are structured to close. Founded by Joshua Douglas, who brings 12+ years in financial crime and CAMS certification, the firm provides fractional CCO and BSA Officer services alongside full program support: policy development, risk assessments, transaction monitoring optimization, and exam readiness — for fintechs and payments companies that need compliance expertise, not just another platform.

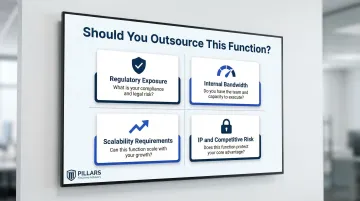

How to Choose the Right Services to Outsource

The right outsourcing decision comes down to one question: what can your internal team not handle reliably at scale — due to capacity constraints, missing expertise, or regulatory depth?

Factors to consider:

- Regulatory exposure: Functions with direct compliance consequences — AML, KYC, data privacy — require partners with verified domain expertise and relevant certifications, not general operational firms. The OCC's 2023 Interagency Guidance on Third-Party Relationships sets clear expectations for how banks and fintechs manage outsourced functions that could affect safety, soundness, or consumer protection.

- Internal bandwidth: If a function is consuming disproportionate internal resources relative to its strategic value, that's a strong signal it should be outsourced.

- Scalability requirements: Customer support, back-office processing, and monitoring operations are strong outsourcing candidates when internal hiring would slow execution during growth phases.

- IP and competitive risk: Core product logic, proprietary risk models, and strategic roadmaps should not be outsourced. Define these boundaries before engaging any partner.

For compliance and financial crime functions specifically, selecting a CAMS-certified advisory partner with hands-on fintech experience—rather than a general BPO or technology vendor—is the difference between a program that holds up under regulatory scrutiny and one that creates liability.

What to Check Before Finalizing an Outsourcing Decision

Before signing with any outsourcing partner, run through these three checks — they separate vendors who look qualified from those who actually are:

- Domain expertise over general capacity: For compliance and financial crime functions, credentials, certifications, and a documented track record with regulators carry real weight. A general BPO may handle volume; it won't handle a regulatory exam.

- Total cost, not just contract cost: The least expensive options often generate expensive downstream problems. Rework after audits, regulatory penalties, or system failures outweigh the initial savings.

- Scalability of the relationship: Outsourcing relationships in fintech evolve as the business scales and regulatory requirements shift. Select partners who can adapt to new obligations — not just execute a fixed deliverable.

Frequently Asked Questions

What are examples of fintech services?

Fintech services include digital payments, mobile banking, peer-to-peer lending, investment platforms, insurance technology, and embedded finance.

What services are commonly outsourced in fintech?

The most frequently outsourced functions include software development, customer support, back-office operations, data analytics, cybersecurity, and compliance/financial crime program management.

What is the most commonly outsourced IT service in fintech?

Software development is the most widely outsourced IT function, particularly for fintechs in early or growth stages. This includes custom application builds, platform integrations, and mobile app development.

What are the 4 types of BPO services?

The four main BPO categories are back-office (accounting, data processing), front-office (customer support, sales), knowledge process outsourcing (analytics, compliance advisory), and IT outsourcing (software development, infrastructure).

Is it safe to outsource compliance functions in fintech?

Outsourcing compliance is safe and common when the partner holds relevant certifications (such as CAMS), has demonstrated experience in fintech regulatory environments, and operates within a clear scope of responsibility with documented ownership.

What should a fintech company look for in a compliance outsourcing partner?

Look for CAMS or equivalent certification, hands-on experience with AML/BSA program design and transaction monitoring, familiarity with regulatory exam preparation, and a track record with fintechs or payments companies rather than general financial institutions.