Introduction

Fintechs face a fundamental tension: rapid growth and product innovation on one side, an increasingly complex web of BSA/AML, KYC, and FinCEN obligations on the other. Every new product, state expansion, or customer segment brings additional regulatory requirements—yet compliance teams built for early-stage operations often can't scale fast enough, turning compliance into a bottleneck rather than an enabler.

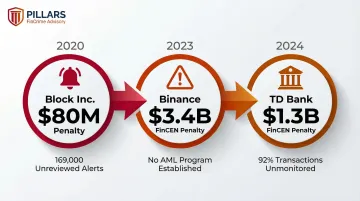

The core problem is operational: lean compliance teams managing manual workflows with spreadsheet-dependent processes that collapse under transaction volume and regulatory scrutiny. When TD Bank paid $1.3 billion to FinCEN in 2024 for systemic transaction monitoring failures—92% of total transaction volume went unmonitored—regulators sent a clear message. Manual processes at scale create exam risk and serious enforcement exposure.

Compliance automation is how modern fintechs close this gap. It frees compliance officers from administrative burden so they can focus on the judgment-intensive decisions that reduce risk.

Key Takeaways

- Compliance automation handles repeatable regulatory tasks like KYC onboarding, transaction monitoring, and regulatory reporting—cutting manual workload and the compliance gaps that come with it

- AI-driven transaction monitoring systems reduce false positives by 30-70%, allowing analysts to focus on genuinely suspicious activity

- Automation requires a well-designed program foundation—automating broken processes scales the problem, not the solution

- Human judgment remains essential for SAR filing decisions, EDD escalations, and complex FinCrime determinations

- Firms like Pillars FinCrime Advisory help fintechs tune transaction monitoring, prepare for exams, and build programs that survive regulatory scrutiny

Why Manual Compliance Is Holding Fintechs Back

At a scaling fintech, manual compliance looks like this: compliance staff reviewing transaction alerts one by one, onboarding queues backing up for days, and quarterly regulatory reports assembled by hand from disconnected systems. This approach creates bottlenecks that slow product velocity, frustrate banking partners, and increase exam risk.

The FinCrime Consequences of Manual Processes

Manual compliance workflows create specific, measurable problems in AML/BSA programs:

- Legacy rule-based transaction monitoring generates 85-95% false positive rates, with analysts spending 30-45 minutes on each alert

- Manual identity verification produces incomplete KYC records — missing beneficial ownership data and undocumented risk decisions

- SAR deadlines slip: Block, Inc. accumulated over 169,000 unreviewed alerts by 2020, filing SARs more than a year after generation

- Audit trails reconstructed after the fact leave programs exposed during regulatory exams and enforcement inquiries

These failures aren't theoretical. FinCEN assessed $3.4 billion against Binance in 2023 for operating over a year with no AML program and ineffective KYC procedures.

The staffing angle is equally instructive. When CommunityBank of Texas paid $8 million in 2021, FinCEN explicitly cited three BSA analysts each averaging 100 case alerts per day — a volume that meant supporting documents routinely went unreviewed before decisions were made.

The Scalability Gap

Each of those failures becomes unavoidable at volume. A fintech processing 50,000 transactions per month can manage manually. At 5 million, the same team structure fails completely. Regulators understand this scaling challenge — and they're penalizing firms that haven't grown their controls alongside their business.

Recent FDIC consent orders against sponsor banks explicitly cite inadequate third-party oversight and BSA/AML program deficiencies related to fintech partnerships. For fintechs relying on sponsor bank relationships, that's a direct threat to their operating model — not just their exam results.

What Is Compliance Automation and Where Does It Apply?

Compliance automation is the use of software and technology to execute regulatory compliance tasks that follow rules-based logic, freeing human reviewers for judgment-intensive decisions. It's not full automation—the goal is structured, consistent execution of repeatable workflows, not replacing compliance officers.

Automated AML Transaction Monitoring

Automated transaction monitoring systems evaluate transactions in real time against behavioral baselines, dollar thresholds, geographic risk flags, and structuring patterns. Batch-review legacy systems process transactions hours or days after they occur. Modern systems analyze activity as it happens.

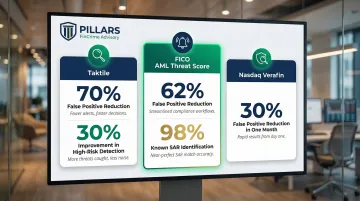

The goal is improving alert quality—surfacing genuinely suspicious activity—not just generating more alerts. AI and machine learning in transaction monitoring consistently reduce false positives at scale:

- Taktile research shows 70% reduction in false positives with 30% improvement in detection of high-risk events

- FICO's AML Threat Score achieved 62% reduction in alert false positives while identifying 98% of known SARs

- Nasdaq Verafin reported 30% decrease in false positive alerts within one month of implementation

These improvements directly reduce the manual review burden. A financial institution processing 10,000 daily alerts at a 90% false positive rate—with 30 minutes per review—burns 4,500 analyst hours per day on non-actionable investigations.

Automated KYC and KYB Onboarding

Automation handles identity verification, sanctions screening, PEP checks, and risk scoring at onboarding—all within seconds rather than hours. Manual KYC takes hours or days due to document follow-ups and human review queues. Automated KYC completes in seconds or minutes using consistent rule-based validation.

KYB specifics for fintechs onboarding business clients:

- Automated beneficial ownership lookups and entity verification

- High-risk flag routing for EDD review

- Consistent, documented records at every step—critical for CDD requirements

FinCEN's 2026 exceptive relief allows financial institutions to bypass re-verifying beneficial ownership information for existing legal entity customers opening new accounts, provided the customer confirms the data remains accurate. This streamlines the automated onboarding process further.

Regulatory Reporting and Audit Trail Automation

Automated SAR/CTR filing workflows, scheduled regulatory reporting, and platforms that timestamp every action and override eliminate the "audit scramble"—the reactive document assembly that consumes teams before regulatory exams.

Real-time audit trails create a defensible record of what happened, when it happened, and who made each decision. During enforcement inquiries, documented automated workflows withstand scrutiny far better than reconstructed manual logs.

Key Benefits of Compliance Automation for Fintechs

Operational Efficiency at Scale

Automation allows a fintech to expand products, enter new states, or increase transaction volume without proportionally growing compliance headcount. The false positive reductions documented earlier translate directly to saved analyst hours—resources that can be redirected to higher-value activities like complex case investigations and risk assessments.

Consistency and Reduced Human Error

Manual compliance is subject to fatigue, personnel turnover, and inconsistent judgment. Automated workflows apply the same rules every time:

- Customer onboarding follows the same process across every account

- Every alert is triaged against the same criteria

- Policy application doesn't vary by analyst, shift, or workload

This consistency is especially important for fintechs with distributed or lean compliance teams where process knowledge may reside with just a few people.

Faster Risk Detection

Automated systems surface suspicious patterns in real time rather than through periodic reviews, reducing the window between a compliance failure and corrective action. In AML contexts, this means identifying structuring attempts, unusual velocity, or high-risk geographic patterns before they escalate into regulatory findings.

Exam Readiness as a Continuous State

The shift from "audit prep mode" to continuous audit readiness changes the regulatory relationship entirely. When every decision is logged, every workflow timestamped, and every exception documented in real time, a regulatory exam becomes a demonstration of a working program—not a reconstruction project.

Competitive and Partnership Credibility

Banking partners, investors, and enterprise clients assess fintech compliance maturity before entering relationships. A structured, automated compliance program with demonstrable controls shortens due diligence timelines and reduces friction in bank sponsor approvals.

Fintechs that can demonstrate real-time monitoring, consistent KYC processes, and complete audit trails are more likely to close banking-as-a-service arrangements and enterprise contracts faster — with fewer conditions attached.

What Compliance Automation Can't Replace

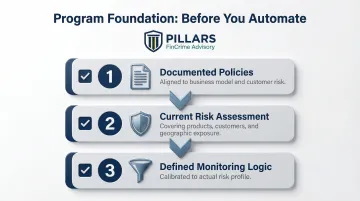

The Program Foundation Must Come First

Automation executes a program—it doesn't design one. A fintech with weak risk assessments, vague AML policies, or mis-scoped transaction monitoring rules will automate those flaws at scale.

Before selecting tools, fintechs need a clear risk-based program foundation:

- Documented policies aligned to business model and customer risk

- Current risk assessment covering products, customers, and geographic exposure

- Defined monitoring logic calibrated to actual risk profile

Firms like Pillars FinCrime Advisory help fintechs build this foundation through program development, risk assessments, and policy design—so automation supports a compliant structure rather than scaling a broken one.

Human Judgment in Complex FinCrime Decisions

Some compliance decisions cannot be delegated to software. The following require experienced human judgment that no automated system can replicate:

- SAR filing decisions where facts are ambiguous or context is sensitive

- Escalated EDD reviews involving high-risk customers or unusual patterns

- Responses to law enforcement inquiries or government subpoenas

- Program-level decisions about control calibration and risk tolerance

Regulators expect automation to support—not replace—qualified compliance oversight.

OCC guidance explicitly states: "A bank's use of third parties does not diminish the responsibility of the bank's board and senior management to ensure that the bank operates in a safe and sound manner and in compliance with applicable laws and regulations."

Regulators hold the institution accountable for outcomes regardless of what the software did. That accountability extends directly into how well the institution can defend its program during an exam.

Regulatory Exam Preparation Requires Strategic Expertise

Passing a regulatory exam requires more than functional software. Examiners want to know how the program works, why controls are calibrated the way they are, and how the firm responded when something went wrong.

Fintechs preparing for FinCEN examinations, state money transmitter audits, or bank sponsor reviews need compliance expertise alongside compliance software. Working with an experienced FinCrime advisory partner like Pillars FinCrime Advisory helps firms translate their automated controls into a coherent, defensible program narrative before examiners ask the hard questions.