Introduction

Cross-border digital payments are scaling fast—flows reached approximately $150 trillion in 2022 and approached $1 quadrillion in 2024. That growth has drawn intensifying regulatory scrutiny from multiple directions at once. The consequences of non-compliance go beyond fines: frozen accounts, license suspension, and reputational damage that can take years to recover from.

Unlike domestic payments, cross-border digital transactions touch multiple jurisdictions, each with its own AML standards, licensing requirements, data protection laws, and sanctions regimes. A single payment can cross three countries, each governed by a different regulatory framework. Most fintechs and payments companies don't fully grasp that burden until they're sitting across from an examiner.

This guide covers the key regulatory frameworks governing cross-border digital payments, the three non-negotiable compliance pillars (KYC, AML, and sanctions screening), common pitfalls, red flags, and how to build a program that holds up under regulatory examination.

TLDR

- Cross-border payments must comply with overlapping rules from FATF, OFAC, FinCEN, and regional frameworks like PSD2 and AMLD6

- KYC, AML, and sanctions screening are non-negotiable cornerstones of any defensible compliance program

- Real-time payment rails compress the time available for compliance review, raising the stakes for proactive monitoring

- Structuring, round-tripping, and high-risk corridor exposure require continuous monitoring

- Audit-ready programs are built on documented policies, tuned transaction monitoring, and regular review cycles

Why Cross-Border Digital Payments Carry Elevated Compliance Risk

The Multi-Jurisdictional Problem

A single cross-border transaction can pass through several countries, each governed by its own AML regulations. Gaps between standards create loopholes that bad actors exploit. Compliance teams must account for all legs of the payment chain—not just the originating jurisdiction.

When a payment moves from the U.S. through the EU to Singapore, it must satisfy:

- FinCEN requirements under the U.S. Bank Secrecy Act

- AMLD6 provisions governing EU member states

- MAS regulations applicable in Singapore

Intermediary banks and payment processors sitting between originator and beneficiary can truncate or omit key data fields, making accurate sanctions screening and risk assessment difficult. Incomplete ISO 20022 adoption compounds this problem—when payments move between ISO 20022 (MX) and legacy (MT) formats mid-chain, structured information is often lost or truncated, leaving data gaps across many corridors.

Speed Compounds the Risk

Real-time and near-instant payment rails compress the review window for compliance teams. Unlike batch processing, real-time flows leave little room to intervene before funds have moved. Proactive monitoring becomes essential—reactive investigation after the fact is rarely effective. Sanctions screening and transaction monitoring systems must operate at machine speed to keep pace with real-time settlement.

As of 2024, 76% of Fast Payment Systems process ISO 20022 messages, but the coexistence of legacy formats creates interoperability delays and data truncation risks during cross-border routing.

Key Regulatory Frameworks for Cross-Border Digital Payments

Navigating cross-border payments means operating under multiple overlapping regulatory regimes simultaneously. Understanding each framework — and where they intersect — is essential for building a compliant program.

FATF and the Travel Rule

The Financial Action Task Force (FATF) sets the baseline international standards that most jurisdictions implement domestically. FATF Recommendation 16 (the Travel Rule) requires collection and transmission of originator and beneficiary information for wire transfers.

The June 2025 update standardized requirements for peer-to-peer cross-border payments above $1,000 (USD/EUR), requiring name, address, and date of birth. The scope now extends to virtual asset transfers, directly impacting digital payment providers and Virtual Asset Service Providers (VASPs).

Jurisdiction-Specific Frameworks to Know

United States

The U.S. regulatory framework centers on three primary regulators:

FinCEN: Enforces AML program requirements, SAR and CTR filing obligations, and beneficial ownership rules under the Corporate Transparency Act.

- MSBs must maintain written AML programs and file SARs for transactions aggregating at least $2,000 suspected to involve illegal activity

- CTRs are required for currency transactions over $10,000

OFAC: Enforces economic sanctions with strict civil penalties. The 2025 maximum for IEEPA violations is $377,700 per violation (or twice the transaction amount).

OFAC SDN List: Updated frequently and at random, sometimes daily — continuous screening is a practical necessity, not optional.

Bank Secrecy Act: The foundational compliance law establishing recordkeeping and reporting requirements.

European Union and United Kingdom

PSD2: Requires Strong Customer Authentication for remote electronic payments and establishes open banking obligations.

Wire Transfer Regulation (2015/847): Requires transfers to be accompanied by payer and payee information, including name, account number, and address or date of birth.

AMLD6: Expands predicate offenses for money laundering to 22 categories (including cybercrime and tax crimes) and establishes criminal liability for legal persons (corporations).

GDPR: Data minimization and transfer restrictions affect how KYC data can be shared cross-border.

Asia-Pacific and Other Key Markets

Singapore: The Payment Services Act requires a Major Payment Institution license if average monthly transactions exceed S$3 million for one service or S$6 million for multiple services.

Brazil: PIX regulation allows non-authorized payment institutions to integrate into the Brazilian Payment System. LGPD requires specific mechanisms (standard contractual clauses, adequacy decisions) for international data transfers.

China: PIPL regulations require security assessment, standard contract, or certification for cross-border personal data transfers unless specific exemptions apply.

FSB's "Same Activity, Same Risk, Same Rules" Principle

The Financial Stability Board's December 2024 recommendations address regulatory arbitrage between bank and non-bank payment service providers. For fintechs and payments companies, the practical implication is clear: the compliance expectations once reserved for banks are increasingly being applied to non-bank providers operating cross-border.

The Three Pillars: KYC, AML, and Sanctions Compliance

KYC, AML, and sanctions screening form the non-negotiable operational core of any cross-border payments compliance program. Weaknesses in any one pillar create systemic risk across the others.

Know Your Customer (KYC) and Know Your Business (KYB)

The first pillar starts with identity — but effective KYC goes well beyond collecting government-issued IDs, proof of address, and business registration documents. It requires risk-tiering customers based on:

- Geographic exposure (high-risk jurisdictions)

- Transaction volume and velocity

- Business type and stated purpose

- PEP status and adverse media exposure

Enhanced Due Diligence (EDD) is required for high-risk relationships. Banks assign 10% to 15% of their full-time equivalents exclusively to KYC/AML operations — a signal of how heavily compliance operations weigh on headcount for fintechs and financial institutions alike.

Beneficial Ownership Verification

Ultimate Beneficial Owner (UBO) verification is now required by regulators across major jurisdictions. Corporate layering and offshore structures remain common tactics for obscuring who actually controls funds.

Compliance teams must look through complex structures to identify the individual(s) in control. Key regulatory drivers include:

- U.S. Corporate Transparency Act — mandates UBO disclosure for most registered entities

- EU beneficial ownership registries — expanded access and verification requirements under AMLD reforms

- FATF Recommendation 24 — the global standard on transparency of legal persons

AML Transaction Monitoring

Effective transaction monitoring for cross-border payments must account for:

- Unusual routing through high-risk jurisdictions

- Rapid movement of funds through multiple accounts

- Structuring patterns (breaking amounts to avoid thresholds)

- Transactions inconsistent with stated business purpose

Rule-based systems alone are insufficient. Models tuned only to domestic baselines will miss the typologies that define cross-border risk — different routing behaviors, jurisdiction profiles, and originator data gaps require distinct calibration.

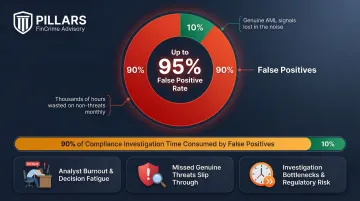

The False Positive Burden

Cross-border payments disproportionately trigger alerts due to name transliteration inconsistencies, incomplete originator/beneficiary data, and geographic risk flags. AML false positive rates typically range between 85% and 95%, consuming up to 90% of compliance investigation time. High false positive rates lead to analyst fatigue, slower investigations, and missed genuine threats.

SAR and CTR Filing Obligations

Under FinCEN rules:

- CTRs are required for currency transactions over $10,000

- SARs must be filed when suspicious activity is detected—for MSBs, the threshold is $2,000

Document the decision-making rationale for regulatory exams. Examiners scrutinize not just whether SARs were filed, but whether the analysis was thorough and well-documented.

Sanctions and PEP Screening

All parties—originator, beneficiary, intermediary institutions, and ultimate beneficial owners—must be screened against:

- OFAC's SDN list

- EU sanctions lists

- UN sanctions committees

- PEP databases

Screening must occur before and during the transaction lifecycle. Free-text fields and payment message fields must also be screened, not just structured data. The OFAC SDN list updates frequently and without warning. Real-time feed integration is non-negotiable — periodic manual updates create exposure gaps that examiners will find.

Common Compliance Challenges—and How to Overcome Them

The Technology Gap

Many financial institutions and payments companies still rely on manual or legacy compliance processes. Global spending on third-party AML systems is projected to grow 121% to surpass $75 billion globally by 2030, up from $33.9 billion in 2025. Manual processes cannot scale with transaction volume or real-time payment speeds.

Data Inconsistency Challenges

Even with ISO 20022 being adopted as the global messaging standard, uneven implementation means incoming payment data is often incomplete or inconsistently formatted. Compliance teams need processes that flag missing fields without blocking legitimate payments or passing risky ones through.

Shifting Sanctions Landscape

Sanctions regimes are updated frequently by OFAC, the EU, the UN, and regional authorities. Compliance teams relying on periodic list updates rather than real-time feed integration are chronically behind. The risk is concrete: a transaction that was compliant at 9 a.m. can violate sanctions by noon if a new designation is issued.

Cost Management

Average annual spend on AML/KYC operations stands at $72.9 million per firm globally. Yet the cost of non-compliance far exceeds the cost of investing in scalable compliance infrastructure. Global regulatory penalties totaled $3.8 billion in 2025, including FinCEN's $1.3 billion penalty against TD Bank for willfully failing to implement an adequate AML program.

Advisory partners like Pillars FinCrime Advisory specialize in exactly this: helping fintechs and payments companies build programs that are practical and right-sized for their risk profile and growth stage.

Multi-Jurisdictional Governance

Operating across jurisdictions requires building internal governance that documents how compliance decisions are made. Regulators expect evidence of:

- Model risk assessments

- Alert tuning rationale

- Analyst training records

- SAR decision logs

Regulators treat missing documentation as a compliance failure in its own right, regardless of whether the underlying controls are sound.

Red Flags in Cross-Border Digital Transactions

Transaction and Behavioral Red Flags

Monitor for these transaction-level indicators:

- Structuring: Numerous transactions just under reporting thresholds (e.g., $9,500) followed by international wire transfers

- Round-tripping: Transactions that return to the originator after passing through foreign accounts

- Round-number transactions: Payments in suspiciously even amounts that lack a clear invoice or business rationale

- Inconsistent patterns: Transaction volume or destinations that don't align with stated business purpose or historical behavior

- Rapid layering: Quick movement through multiple countries with no clear business rationale

Customer behavior red flags include:

- Sudden increase in international transfers without explanation

- Reluctance to provide KYC documentation or counterparty information

- Multiple foreign accounts with no apparent operational purpose

- Use of complex corporate structures or nominee directors to obscure beneficial ownership

Geographic and Counterparty Red Flags

Geographic exposure adds another layer of risk that transaction-level signals alone won't capture. Flag payments involving any of the following:

- Jurisdictions on the FATF high-risk and monitored list

- OFAC-sanctioned countries or regions

- Offshore financial secrecy havens with limited transparency requirements

- Countries with high corruption index scores (Transparency International's CPI is a standard reference)

Geographic risk must be factored into customer risk scoring and transaction monitoring thresholds—not treated as a binary block/allow decision.

Building an Audit-Ready Cross-Border Payments Compliance Program

Foundation: Written, Risk-Based Policies

A defensible program starts with a written, risk-based compliance policy specific to the organization's payment corridors, customer base, and business model. Generic policies copied from templates are a common examination failure point. FinCEN requires four minimum pillars:

- Internal policies, procedures, and controls

- Independent audit function to test programs

- Designated compliance officer

- Ongoing employee training program

Review and update policies at least annually, or whenever business model or regulatory changes occur.

Operational Controls

A well-structured cross-border payments compliance program includes:

- Documented KYC/KYB procedures with clear risk-tiering criteria and EDD triggers

- Calibrated transaction monitoring system with clear alert escalation paths

- Sanctions screening with real-time list updates

- SAR/CTR filing workflow with documented decision logs

- Designated ownership for each component subject to quality assurance review

Audit Readiness and Independent Review

Internal audits should be conducted annually, with external reviews every two years or more frequently during periods of regulatory change or business expansion. The FFIEC BSA/AML Examination Manual emphasizes that independent testing must sufficiently cover ML/TF risks. Violations, exceptions, or deficiencies must be reported to the board promptly and tracked through corrective action.

Beyond outcomes, regulators increasingly scrutinize the reasoning behind decisions — including:

- Model documentation

- Threshold justification

- Training records

- Not just outcomes, but the rationale behind decisions

For fintechs and payment companies scaling quickly, outside advisory support can accelerate audit readiness considerably. Pillars FinCrime Advisory works with growth-stage fintechs and payments companies on the full compliance program lifecycle — from policy development and risk assessments to transaction monitoring optimization and exam preparation.

Frequently Asked Questions

What is the FATF Travel Rule and does it apply to digital payment companies?

FATF Recommendation 16 requires originator and beneficiary information to travel with wire transfers. Its scope has expanded to cover virtual asset service providers and increasingly applies to digital payment providers depending on jurisdiction, especially for transactions above $1,000 USD/EUR.

What are the consequences of non-compliance with cross-border payment regulations?

TD Bank's record $1.3 billion FinCEN penalty in 2024 illustrates the stakes. Consequences include OFAC fines up to $377,700 per violation, license suspension, transaction freezes, reputational damage, and in severe cases, criminal liability for individuals.

What is the difference between KYC and KYB in cross-border payments?

KYC (Know Your Customer) verifies individual customer identity and risk profile. KYB (Know Your Business) verifies the identity, structure, and beneficial ownership of corporate entities. Both are required for business-to-business cross-border payment relationships.

How often should a cross-border payments compliance program be audited or reviewed?

Conduct annual internal audits and biennial external reviews at a minimum. Additional reviews should be triggered by regulatory changes, new market expansion, significant transaction volume growth, or examination findings.

What licenses do fintech and payments companies need for cross-border transactions?

Requirements vary by jurisdiction. Common examples include:

- U.S.: FinCEN MSB registration plus state money transmitter licenses

- EU/UK: Payment Institution or E-Money Institution license

- Singapore: MAS Major Payment Institution license

Operating without the appropriate license is itself a regulatory violation.

What are the biggest AML red flags specific to cross-border digital payments?

Key red flags include:

- Structuring across multiple jurisdictions

- Rapid layering through high-risk corridors

- Mismatch between transaction purpose and customer profile

- Payments involving sanctioned or high-risk jurisdictions

- Round-tripping and vague remittance information