Introduction

Regulatory expectations for KYC are rising across every major jurisdiction, while customer volumes, cross-border transactions, and geographic complexity continue to surge. Most compliance programs were designed for a single market and a manageable customer base — they were never built to handle both pressures at once.

The cost of failing this test is severe. TD Bank paid $3 billion in 2024 for systemic transaction monitoring breakdowns. Binance faced $4.3 billion in penalties for allowing users to trade with only an email and failing to file SARs. Global AML enforcement reached $4.6 billion in 2024, with regulators squarely focused on systemic failures — not policy gaps, but programs that don't actually function as intended.

This guide covers what global banks must navigate to build KYC programs that scale without breaking:

- The regulatory landscape spanning FATF, the US, EU/UK, APAC, and emerging markets

- Structural components of a KYC program designed for scale

- The most common failure points as programs grow

- What separates programs that hold up under regulatory scrutiny from those that don't

Key Takeaways

- KYC compliance is an ongoing, risk-based program encompassing identity verification, due diligence, screening, monitoring, and recordkeeping — not a one-time check.

- Global banks must satisfy FATF baselines plus jurisdiction-specific rules across the US, EU/UK, APAC, and emerging markets, each with distinct documentation and data privacy requirements.

- Weak policy and governance foundations are the primary reason KYC programs fail to scale — technology cannot compensate for structural gaps in risk tiering or controls design.

- Build in layers: sound policy architecture first, risk-based workflows second, technology automation third.

- Fintechs and payments companies building from scratch benefit most from structured program design before deploying technology — Pillars FinCrime Advisory supports that process from policy development through transaction monitoring optimization.

What KYC Compliance Actually Demands of Global Banks

KYC compliance is a continuous, risk-based program — not a static identity check at account opening. Regulators evaluate whether your program actually works: does it detect risk, escalate appropriately, and produce defensible documentation? Without accurate customer identification and risk profiling, transaction monitoring and suspicious activity detection cannot function.

The universal regulatory expectation is a risk-based approach: calibrate due diligence, monitoring, and controls to the assessed risk of each customer, product, and geography rather than applying uniform treatment across all accounts. This lets you concentrate resources where risk is highest while keeping lower-risk segments operationally efficient. In a compliance context, "scalable" means maintaining consistent quality and regulatory defensibility as volumes, product lines, and geographies expand — without proportionally scaling headcount or creating unmanageable friction.

Five Regulatory Expectations That Define a Functioning KYC Program

- Written, board-approved policies covering CIP, CDD, EDD, screening, and monitoring requirements

- A designated compliance officer with clear authority and accountability to senior management

- Periodic independent testing to identify control gaps and measure program effectiveness

- Role-specific staff training on red flags, escalation procedures, and regulatory requirements

- A structured CDD framework that assesses, documents, and monitors customer risk throughout the relationship

Regulators look for evidence these work in practice, not just on paper. FinCEN's 2024 NPRM explicitly requires that AML programs be "effective, risk-based, and reasonably designed" — a shift from technical compliance to outcome-based supervision. That shift has direct enforcement consequences.

The Enforcement Reality

Transaction monitoring failures accounted for $3.3 billion in enforcement actions in 2024, the largest share of the $4.6 billion total. Regulators are punishing systemic breakdowns: programs that fail to monitor activity, miss obvious suspicious patterns, or file hundreds of late SARs. Non-compliance risk has materially increased, and regulators are focused on outcomes — whether your program actually mitigates illicit finance risk — not just whether policies exist.

Navigating the Global Regulatory Landscape

FATF (Financial Action Task Force) sets the global baseline standards for AML/KYC. Most national regulatory frameworks derive from or align to FATF Recommendations. But each jurisdiction adds its own documentation requirements, reporting obligations, beneficial ownership rules, and enforcement thresholds.

FATF comprises 39 member countries and 9 FATF-Style Regional Bodies, with the Russian Federation's membership suspended. While technical compliance may rate highly in specific samples — 100% of a recent four-jurisdiction sample rated Largely Compliant on Recommendation 10 (Customer Due Diligence) — FATF mutual evaluations frequently note that effectiveness in practice remains a challenge, particularly for Designated Non-Financial Businesses and Professions.

United States

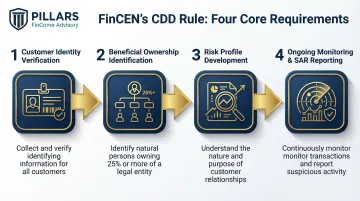

The US regulatory framework is built on the Bank Secrecy Act (BSA), the USA PATRIOT Act, and FinCEN's CDD Rule. The CDD Rule has four core requirements:

- Identify and verify customer identities

- Identify and verify beneficial owners of companies opening accounts (25% ownership threshold)

- Understand the nature and purpose of customer relationships to develop risk profiles

- Conduct ongoing monitoring to identify and report suspicious transactions and maintain updated customer information

Currency Transaction Reports (CTRs) must be filed for transactions exceeding $10,000. Suspicious Activity Reports (SARs) must be filed no later than 30 calendar days after initial detection, with an additional 30-day extension allowed if no suspect is identified — but never more than 60 days total. The Travel Rule requires recordkeeping for funds transfers of $3,000 or more.

The 2025 Corporate Transparency Act Reversal: In March 2025, FinCEN exempted all U.S. domestic entities and U.S. persons from BOI reporting requirements, shifting the burden entirely to foreign reporting companies. Foreign entities registered before March 26, 2025, had until April 25, 2025, to file; those registered after have 30 days from registration notice.

Multiple federal agencies and state regulators share enforcement authority. FinCEN has increasingly focused on outcome-based supervision — whether programs deliver material risk mitigation.

European Union and United Kingdom

Recent EU directives have progressively tightened the framework:

- AMLD5 required Member States to establish beneficial ownership registers and lowered thresholds for anonymous prepaid cards

- AMLD6 expanded criminal liability to legal persons and harmonized predicate offenses, including cybercrime and environmental crime

- AMLA launches in Frankfurt in mid-2025 with 400+ staff, direct supervisory powers over high-risk institutions, and authority to impose pecuniary sanctions

In the UK, the Financial Conduct Authority supervises banks and cryptoasset businesses under the Money Laundering Regulations 2017. The FCA employs a data-led supervisory approach and expects firms to conduct risk assessments, apply due diligence, and appoint a Money Laundering Reporting Officer.

GDPR and UK GDPR Constraints: Layered on top of these supervisory requirements, cross-border KYC data sharing must navigate strict data minimization and purpose limitation rules. International transfers to third countries require adequate safeguards — adequacy decisions or binding corporate rules — complicating global KYC workflows.

Asia-Pacific and Emerging Markets

Singapore's MAS Notice 626 and Hong Kong's HKMA guidance set stringent benchmarks for risk-based CDD and enhanced due diligence. Both frameworks expect institutions to document how their control intensity aligns with customer risk classifications — not simply apply uniform procedures.

That level of regulatory maturity is far from uniform across the region. Elsewhere in APAC, and across LATAM and Middle East/Africa markets, FATF alignment is improving — but uneven supervision and enforcement still create meaningful risk management challenges for correspondent banking and cross-border exposure. For example, Brazil's 2023 FATF MER rated the country Partially Compliant on Recommendation 22, noting major deficiencies in CDD implementation by DNFBPs and insufficient beneficial ownership identification for legal arrangements.

The Core Components of a Scalable KYC Program

A scalable KYC program is a structured, documented workflow where each component depends on the one before it. When any layer is weak — identification, due diligence, screening, or monitoring — the gaps compound. What breaks under volume pressure is rarely one thing; it's the point where an underdocumented process meets examiner scrutiny.

Customer Identification Program (CIP)

CIP establishes the legal obligation to collect and verify basic customer information — name, date of birth, address, government-issued ID — before account opening. It must be documented in policy, applied consistently, and tested. Gaps at this stage create errors that compound through due diligence and monitoring.

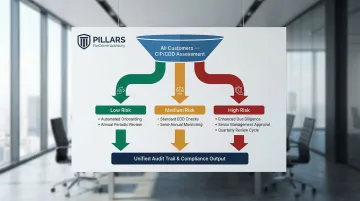

Customer Due Diligence (CDD) and Risk Scoring

CDD requires understanding the customer's business or occupation, source of funds, expected account activity, and geographic exposure — then assigning a risk rating that drives the level of ongoing monitoring required.

Risk scoring methodology must be:

- Documented — Clear criteria for each risk tier

- Consistently applied — Same factors assessed for all customer types

- Defensible to examiners — Rationale and data supporting each rating

Enhanced Due Diligence (EDD)

EDD applies to high-risk customers: those in high-risk jurisdictions, industries, or ownership structures — including complex beneficial ownership chains, PEPs, and correspondent banking relationships.

EDD typically requires:

- Deeper documentation of source of funds and wealth

- Senior management approval before account opening

- More frequent periodic reviews (quarterly or semi-annually vs. annually)

- Additional transaction monitoring controls

A clear, documented EDD trigger framework is essential for scalability. Without it, frontline staff apply EDD inconsistently, creating both compliance gaps and operational bottlenecks.

PEP and Sanctions Screening

Institutions must screen all customers against global sanctions lists and Politically Exposed Person (PEP) databases at onboarding and on an ongoing basis.

The challenge at scale: False positives. Name-matching limitations, transliteration issues across languages, and low-quality data sources generate high alert volumes. Celent reports that AML and fraud false positive rates hover between 85% and 99%, with each alert consuming 5 to 30 minutes — or hours if escalated.

Effective screening programs require both quality data sources and a structured process for resolving alerts that avoids analyst fatigue.

Ongoing Monitoring, Periodic Reviews, and SAR Filing

KYC does not end at onboarding. Institutions must:

- Monitor transaction activity against the customer's established risk profile

- Trigger periodic reviews — especially for higher-risk accounts — to verify information remains current and accurate

- Escalate suspicious activity through Suspicious Activity Reports (SARs)

Monitoring thresholds set at onboarding rarely stay accurate as customer behavior evolves. Without regular tuning tied to risk tier, alert volumes grow, analyst capacity gets consumed by noise, and genuine risk takes longer to surface — the opposite of what a scalable program is supposed to achieve.

Why Global Banks Struggle to Scale KYC Compliance

Most KYC programs were designed for a single jurisdiction and a manageable customer volume. As banks expand globally, fragmentation multiplies across document types, data privacy rules, risk profiles, and regulatory expectations — while the underlying program architecture was never built to handle that complexity.

The cost of maintaining these programs is significant. In 2023 alone:

- U.S. and Canada financial crime compliance costs hit $61 billion, driven primarily by labor

- EMEA costs reached $85 billion, with 72% of organizations reporting increases

- UK firms averaged £188 million annually on financial crime compliance, with 66% directed toward customer due diligence

The False Positive Spiral

Automated transaction monitoring and screening systems calibrated for one market or customer base produce high volumes of false alerts when applied to a larger, more diverse population. Each unresolved false positive consumes analyst resources that should focus on genuine risk. The problem compounds as customer volumes grow.

Large banks employing thousands of compliance staff see average employees making 10 to 30 errors per 100 opportunities. Those errors often trace back to poorly tuned models — one of the most common findings in regulatory examinations. Metro Bank was fined £16.7 million after its automated transaction monitoring system failed to track over 60 million transactions due to data input errors.

The Governance Gap That Emerges at Scale

When KYC policies are written for compliance checkboxes rather than operational guidance, frontline staff apply them inconsistently — across geographies where regulatory interpretations vary. Without documented, regularly tested procedures and a clear escalation framework, quality degrades as volume increases. That degradation is precisely what draws regulatory enforcement action.

How to Build a KYC Program That Scales Without Breaking

Technology cannot scale a broken program. Before investing in automation, institutions must ensure their policy infrastructure is documented, their risk tiers are defined and defensible, their controls are consistently applied, and their audit trail is complete.

Establish a Program-Ready Baseline

A program-ready baseline includes:

- Documented CIP/CDD/EDD procedures with clear triggers and workflows

- A written risk assessment that reflects your actual customer base, product risk, and geographic exposure

- Defined escalation paths for alerts, suspicious activity, and policy exceptions

- A training framework that ensures frontline staff understand procedures and apply them consistently

Use Risk Tiering as the Operational Engine of Scalability

When customers are accurately segmented by risk level, institutions can automate high-volume, low-risk pathways and concentrate human review on cases that actually warrant it.

A well-designed risk tier framework:

- Reduces operational friction by routing routine cases through streamlined processes

- Lowers false positive rates by applying appropriate monitoring thresholds to each tier

- Gives examiners the documented rationale they look for during reviews

Deploy Technology on Top of Sound Foundations

AI/ML-driven transaction monitoring, automated PEP/sanctions screening, digital identity verification, and workflow automation tools increase throughput and consistency — but only when deployed on top of sound policy and governance foundations.

Real-world AI/ML performance gains:

- Valley National Bank reduced monthly AML alert volumes by 22% and false positives by over 30% using ML

- HSBC achieved a 20% reduction in false AML alerts

- AI/ML tools can predict whether an alert is a false positive with 99% accuracy

However, regulators demand rigorous model governance. OCC Bulletin 2021-19 explicitly applies SR 11-7 Model Risk Management standards to BSA/AML systems, requiring effective challenge, independent validation, and ongoing monitoring.

That model governance requirement is driving another structural shift: convergence of KYC, fraud, and AML signals into unified compliance platforms. By breaking down data silos, institutions can apply shared analytics to assess both the individual and the transaction in real time — reducing false positives and compressing onboarding timelines simultaneously.

For fintechs and payments companies building programs from the ground up, advisory expertise in program design is often the fastest path to an audit-ready foundation. Pillars FinCrime Advisory provides end-to-end support, from policy development and risk assessments to transaction monitoring optimization and audit preparation.

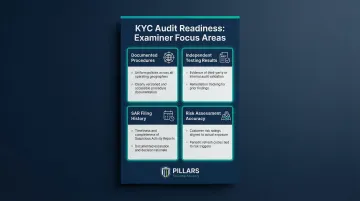

Build Audit Readiness Into Your Operational Rhythm

Audit readiness is an ongoing discipline, not a pre-examination scramble. Examiners look for:

- Documented procedures applied consistently across geographies and customer types — not just written down, but followed

- Independent testing results: audit reports, validation findings, and tracked remediation

- A SAR filing history showing timely submissions, accurate narratives, and appropriate escalation

- A risk assessment that maps to your actual customer base, product mix, and geographic footprint — not a boilerplate template

Institutions that treat audit readiness as a standing operational practice — rather than a reactive sprint — consistently show examiners a program that runs itself, not one that was assembled for the occasion.

Frequently Asked Questions

What is KYC compliance in banking?

KYC compliance in banking is the legal and regulatory requirement for financial institutions to verify customer identities, assess the risk they pose, and monitor their activity on an ongoing basis, as part of a broader AML program designed to prevent financial crime.

What is the $3,000 bank rule?

The $3,000 rule refers to FinCEN's requirement under the Bank Secrecy Act that banks collect and retain records for funds transfers of $3,000 or more, including the originator and beneficiary's name and address. This is separate from the $10,000 CTR filing threshold.

How do global banks scale KYC operations without sacrificing compliance quality?

Scalable KYC programs rely on three interdependent elements: a documented policy and governance foundation, a risk-tier framework that routes customers to the appropriate level of scrutiny, and technology automation that handles high-volume routine checks, freeing skilled analysts for complex, high-risk cases.

What are the biggest KYC compliance challenges for global banks?

Global banks face four recurring pressure points:

- Navigating divergent regulatory requirements across jurisdictions

- Managing false positive volumes from transaction monitoring and screening systems

- Applying policies consistently across geographies

- Keeping beneficial ownership documentation current for complex corporate structures

What is enhanced due diligence (EDD) and when is it required?

EDD is a heightened level of scrutiny applied to high-risk accounts, typically triggered by factors like PEP status, complex ownership structures, high-risk jurisdictions, or unusual transaction patterns. It requires deeper documentation, senior management sign-off, and more frequent reviews than standard CDD.

How does a risk-based approach to KYC help banks manage cross-border compliance?

A risk-based approach concentrates intensive compliance resources on the customers, products, and geographies that present the highest risk, rather than applying uniform scrutiny across all accounts. This improves operational efficiency and regulatory defensibility, especially when operating across jurisdictions with varying risk profiles.