How to Select Compliance Automation Solutions: Best Practices

Compliance obligations are expanding, regulators are intensifying scrutiny, and manual processes can no longer keep pace with the volume and complexity of financial crime risk. For fintechs, payments companies, and financial institutions, automation isn't optional anymore — the real challenge is choosing the right solution.

Selecting the wrong compliance automation tool creates more operational friction, not less. The right choice means matching technology capabilities to your specific regulatory environment, risk profile, and program maturity — not defaulting to the vendor with the most features or the most aggressive sales pitch.

This guide covers the key factors to evaluate when selecting a compliance automation solution:

- How to assess your current program maturity before evaluating vendors

- Which core capabilities to prioritize for AML, KYC, and transaction monitoring

- How to evaluate integration requirements and scalability

- Red flags to watch for during vendor due diligence

- How to build an internal business case for the investment

Key Takeaways

- Effective compliance automation covers AML/BSA workflows, transaction monitoring, and examiner-ready documentation

- Begin with a clear understanding of your regulatory obligations and program gaps, not with a software demo

- Evaluate regulatory coverage, alert quality, system integration, scalability, audit trail robustness, and vendor expertise

- Prioritize FinCrime-specific platforms over generic GRC tools—they're built for the workflows financial institutions actually face

- An experienced advisor bridges the gap between vendor claims and real-world compliance performance

What is Compliance Automation in Financial Crime?

Compliance automation in the financial crime context means using technology to continuously monitor, enforce, and document controls required under AML/BSA regulations, FinCEN guidance, OFAC requirements, and related frameworks. It replaces manual, reactive processes with systematic, audit-ready workflows that hold up under regulatory examination.

This goes well beyond generic governance, risk, and compliance (GRC) platforms. Financial crime compliance automation spans transaction monitoring systems, case management tools, customer risk scoring engines, and automated SAR/CTR filing workflows, each built to handle the specific requirements of AML/BSA programs.

Key Use Cases in FinCrime Programs

Automation applies across the entire financial crime program lifecycle:

- Onboarding and KYC/CDD screening – Verifying customer identities and beneficial ownership at account opening

- Ongoing transaction monitoring – Detecting unusual patterns and potential money laundering typologies in real time

- Alert triage and case management – Managing alerts, investigations, and decision documentation systematically

- Regulatory reporting – Filing SARs, CTRs, and other required reports accurately and on time

- Exam preparation – Producing tamper-evident audit trails and documentation for regulatory reviews

The underlying objective is consistent, defensible control execution — the kind regulators can trace, test, and verify during an examination.

Why Financial Institutions Are Turning to Compliance Automation

Regulatory pressure is the primary driver. FinCEN assessed a record $1.3 billion penalty against TD Bank in 2024 for willful violations of the Bank Secrecy Act, including failure to monitor trillions of dollars in transactions and failure to file SARs on approximately $1.5 billion in suspicious activity. The OCC added a concurrent $450 million penalty for the same systemic breakdowns. FinCEN, the OCC, and state banking agencies are all conducting more frequent exams and holding programs to a higher standard.

Manual transaction monitoring at scale creates operational challenges that compliance teams can no longer ignore:

- False positive rates routinely reach 90% to 95%, overwhelming analysts with unproductive work

- Analysts spend 80% to 85% of their time gathering data and documenting reviews rather than analyzing risk

- Inconsistent documentation creates red flags during regulatory exams

These pressures hit fintechs and payments companies especially hard. Rapid customer growth can outpace manual compliance capacity almost overnight — and the transaction volumes involved are staggering. Zelle processed 3.6 billion transactions totaling over $1 trillion in 2024, a 25% year-over-year increase.

The ACH Network processed 33.6 billion payments in 2024, valued at $86.2 trillion. At that scale, manual processes don't just create inefficiency — they create regulatory exposure.

Key Factors to Consider When Selecting a Compliance Automation Solution

No single solution fits every organization. The right tool depends on your regulatory obligations, existing infrastructure, program maturity, and growth trajectory. The factors below help translate those variables into a structured evaluation framework.

Regulatory Framework Coverage and Specificity

A solution designed for SOC 2 or GDPR compliance operates differently from one built to support BSA/AML, OFAC screening, or FinCEN's Customer Due Diligence rule. Generic tools often miss the specificity that financial crime compliance requires.

Verify that any tool under consideration explicitly covers the regulatory frameworks applicable to your charter, license type, and customer base.

Why this matters: Gaps in regulatory coverage create blind spots likely to surface during an exam, exposing the organization to findings, consent orders, or civil money penalties. The FFIEC BSA/AML Examination Manual requires that automated monitoring systems cover multiple transaction types and that filtering criteria be tailored to the bank's specific higher-risk products, services, customers, and geographies.

Transaction Monitoring Quality and Alert Management

Alert volume and quality are the defining performance metrics for transaction monitoring automation. A tool that generates more alerts doesn't improve compliance—it amplifies analyst workload. Evaluate whether the solution enables tuning, reduces false positives, and supports risk-based alert segmentation.

Benchmark these KPIs:

- Alert-to-SAR conversion rate – Industry sources report approximately 3-5% of alerts result in a SAR

- Mean time to disposition – How quickly alerts are investigated and closed

- Percentage of alerts escalated versus closed – Measures the efficiency of initial triage

Look for vendors who can demonstrate these outcomes, not just feature lists. The Federal Reserve's SR 11-7 guidance requires periodic review and testing of filtering criteria, independent validation of programming methodology, and ongoing monitoring to ensure effectiveness.

System Integration and Data Connectivity

Data access determines what a compliance tool can actually do. Evaluate whether the tool integrates with your core banking system, payment rails, CRM, and case management platform through documented APIs, and whether data flows are reliable and auditable.

Poor integration has a compounding effect. Siloed data creates:

- Inconsistent customer risk profiles across systems

- Missed typology patterns that span multiple data sources

- Manual reconciliation work that defeats the purpose of automation

The tool must pull transaction data, customer information, and screening results in real time to produce accurate risk assessments.

Scalability and Adaptability to Evolving Risk

Fintechs and payments companies face rapid, unpredictable growth. Customer volumes, product lines, and transaction complexity can shift fast. The chosen solution must scale without requiring a full system replacement or manual rule reconfiguration every time a new product launches.

Adaptability requirement: As financial crime typologies evolve—such as crypto exposure, real-time payments fraud, or synthetic identity schemes—the system's detection logic and risk models must be updatable without extended vendor dependency cycles. FinCEN's 2024 Financial Trend Analyses highlight emerging risks including identity-related suspicious activity (1.6 million SARs in 2021), use of convertible virtual currency for human trafficking, and elder financial exploitation.

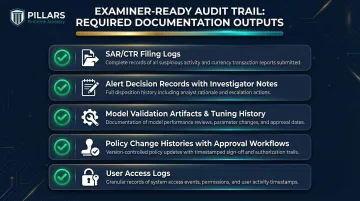

Audit Trail Integrity and Exam Readiness

Regulatory examiners evaluate not just whether controls exist, but whether they were consistently applied and documented. The solution must produce tamper-evident, timestamped audit trails that demonstrate control performance across the entire review period.

Assess specific documentation outputs:

- Automated SAR/CTR filing logs

- Alert decision records with investigator notes and disposition rationale

- Model validation artifacts and tuning history

- Policy change histories with approval workflows

- User access logs showing who reviewed what and when

Ask vendors to show actual examiner-ready output, not sample dashboards. The OCC's consent order against TD Bank cited failure to maintain adequate documentation supporting the methodology for establishing and adjusting rules, thresholds, and filters.

Vendor Expertise, Support, and Implementation Track Record

The vendor's background matters as much as their feature set. A vendor with deep financial crime compliance expertise will configure their solution differently than one serving IT security or general GRC markets.

Before selecting a vendor, ask:

- Whether their team includes CAMS-certified professionals, former BSA officers, or individuals with exam experience

- For references from comparable institutions — fintechs, payments companies, or community banks of similar size

- Specifically about time-to-value and what post-launch support looks like in practice

Poor onboarding, misconfigured rules, and insufficient training are leading causes of compliance automation failures. Vet the implementation track record as rigorously as the product itself.

How Pillars FinCrime Advisory Can Help

Selecting a compliance automation solution is a high-stakes decision. Pillars FinCrime Advisory brings hands-on financial crime expertise to help fintechs, payments companies, and financial institutions evaluate options, identify gaps, and implement solutions that are audit-ready from day one.

Pillars' advisory role covers the entire selection and implementation process. That includes risk assessments that pinpoint where automation delivers the most value, evaluating vendor claims against real-world AML/BSA requirements, and optimizing transaction monitoring rules post-implementation to improve alert quality and reduce operational friction.

Here's what that support looks like in practice:

- Full lifecycle financial crime program support: policy development, risk assessments, transaction monitoring optimization, and exam readiness

- CAMS-certified expertise with 12+ years in financial crime and nearly 20 years across financial services

- Practical, data-driven recommendations built to scale alongside your business, not generic frameworks retrofitted to your program

Conclusion

The right compliance automation solution isn't the most feature-rich or the most widely marketed—it's the one that aligns with your regulatory obligations, integrates with your existing infrastructure, and produces documentation that holds up under examiner scrutiny.

Automation supports your compliance program—it doesn't replace it. The technology must be configured, monitored, and periodically re-evaluated as your business grows and regulatory expectations shift. A solution that works today may need recalibration tomorrow, especially in the fast-moving AML and BSA landscape fintechs and payments companies operate in.

Frequently Asked Questions

What is the difference between a GRC platform and a compliance automation solution for financial crime?

GRC platforms manage broad governance and risk workflows across industries, while FinCrime-specific compliance automation tools are built to handle AML/BSA controls, transaction monitoring, and regulatory reporting workflows unique to financial institutions. Many organizations use both in tandem, with GRC platforms managing policy workflows and FinCrime tools handling transaction surveillance and SAR filing.

How do I know if my organization is ready for compliance automation?

Readiness depends on having defined compliance policies, documented workflows, and at least a baseline understanding of your regulatory obligations. Organizations that automate before establishing these foundations often replicate broken processes at scale, creating more compliance risk rather than less.

What questions should I ask a compliance automation vendor before signing a contract?

Key areas to probe before signing:

- Regulatory framework specificity and coverage for your charter type

- Integration capabilities with your existing core systems

- Post-implementation support model and escalation paths

- Evidence of alert quality improvements at comparable institutions

- Exam history of their existing clients

Request references from organizations with similar charter types and transaction volumes.

Can a small fintech use the same compliance automation tools as a large financial institution?

Tool selection should match program maturity and transaction volume. Some platforms are designed for enterprise scale and may be cost-prohibitive or over-engineered for early-stage fintechs, while others offer tiered configurations suited to growing programs. Focus on solutions that scale with your business, not just what the largest banks use.

What are the most common mistakes organizations make when selecting compliance automation solutions?

Common pitfalls include:

- Prioritizing price over regulatory coverage

- Excluding compliance staff from the evaluation process

- Assuming the tool will self-configure without internal effort

- Failing to stress-test the vendor's audit trail against real examination scenarios

- Underestimating the integration and training lift required post-implementation

How often should compliance automation tools be reviewed and updated after implementation?

Review tools at least annually — or after any significant regulatory change, product launch, or exam finding. Transaction monitoring rules need ongoing tuning as new typologies emerge, and model validation timelines should follow SR 11-7 and OCC Bulletin 2011-12.