The wrong fit leads to compliance gaps, audit failures, and regulatory sanctions that compound as the business scales. In 2024 alone, US regulators issued 42 BSA/AML enforcement actions totaling $3.3 billion, with 54% targeting institutions under $1 billion in assets. Non-compliant businesses spend 2.7x more on remediation than their compliant peers.

The right fit means a defensible, exam-ready program that keeps pace with growth—and the confidence to face regulatory scrutiny without fear.

Key Takeaways

- A regulatory compliance consultant in the FinCrime space builds, manages, and optimizes AML/BSA compliance programs aligned to regulatory expectations

- FinCrime-specific expertise, CAMS certification, and direct experience with your institution type are non-negotiable criteria

- Look for coverage across the full compliance lifecycle: policy development, risk assessments, transaction monitoring, and exam prep

- Key selection factors: domain expertise, credentials, institution-type experience, proactive approach, scalability, and communication clarity

- Expect your compliance partnership to evolve as your business grows and regulations shift

What Is a Regulatory Compliance Consultant?

A regulatory compliance consultant in the financial crime context is a specialized expert who helps organizations build, maintain, and optimize programs designed to detect, prevent, and report financial crime. This includes AML, BSA, sanctions, and fraud—while satisfying FinCEN, OCC, FDIC, or state-level regulatory requirements.

Not all compliance consultants are created equal. A general compliance consultant might handle HR policies or environmental regulations. A FinCrime-specific consultant understands the unique technical requirements around transaction monitoring, SAR filings, and risk-based program design that generalists aren't equipped to address. When facing FinCEN or OCC scrutiny, this distinction becomes critical.

What Services Do They Typically Provide?

Core service areas include:

- BSA/AML policy writing and compliance program development

- Enterprise-wide risk assessments

- Transaction monitoring tuning and alert optimization

- Gap analyses with actionable remediation planning

- Regulatory exam preparation and readiness support

- Ongoing fractional advisory relationships

Project-based vs. ongoing advisory: Project-based engagements deliver specific outcomes—a one-time gap analysis, policy refresh, or exam prep effort. Ongoing advisory relationships provide continuous support as your business evolves. Determine which fits by assessing your compliance maturity, internal bandwidth, and growth trajectory. Emerging fintechs typically need ongoing support; established institutions may require targeted project work.

Why Fintechs and Financial Institutions Rely on Them

Rapidly growing fintechs and payments companies often lack the specialized FinCrime depth or internal bandwidth to stay ahead of evolving regulatory expectations. A consultant fills that gap without the overhead of a full-time senior hire. You get immediate access to expertise that would otherwise take months to recruit, vet, and onboard.

The data backs this up. A Thomson Reuters Cost of Compliance survey found that 34% of financial services firms outsource all or part of their compliance function. Separately, 50% of Anti-Financial Crime professionals cite lack of skilled resources as a top risk.

Common triggers that push organizations toward outside expertise include:

- Regulatory exam scheduled with limited internal prep capacity

- Rapid product or market expansion outpacing existing compliance infrastructure

- Gaps identified in a recent audit or risk assessment

- No in-house BSA Officer or senior FinCrime leadership

Key Factors to Consider When Choosing a Regulatory Compliance Consultant

Selecting a FinCrime compliance consultant requires evaluating both technical capability and strategic fit. The right criteria help connect a consultant's expertise to measurable program outcomes like exam performance, alert quality, and audit readiness.

These factors are especially relevant for fintechs, payments companies, and financial institutions navigating growth, regulatory scrutiny, and evolving financial crime risk. No single criterion tells the full story — weight them together against your specific operating environment.

FinCrime Domain Expertise

A generalist compliance background won't hold up under FinCEN, OCC, or state regulator scrutiny. You need someone who understands AML typologies, BSA obligations, SAR filing quality, sanctions screening, and transaction monitoring logic at a technical level.

How to assess this expertise during vetting:

- Ask for examples of transaction monitoring optimization work—what alert tuning strategies did they implement?

- Request specific regulatory exam support experience—what findings did they help remediate?

- Probe their familiarity with current FinCEN guidance and examination priorities—can they reference recent NPRMs or enforcement trends?

- Evaluate whether they speak in regulatory generalities or provide concrete, technical details

A consultant with real experience will reference specific exam scenarios, cite guidance by name, and explain their reasoning — not just confirm they're familiar with the topic.

Credentials and Certifications

Certifications like CAMS (Certified Anti-Money Laundering Specialist) signal a verified, industry-recognized level of FinCrime expertise and commitment to the field. With over 65,000 CAMS-certified professionals globally, the credential represents a baseline standard for competence.

Treat the absence of relevant credentials as a meaningful risk signal. While the FFIEC BSA/AML Examination Manual doesn't mandate specific certifications, it requires the BSA compliance officer to be "competent, as demonstrated by knowledge of the BSA and related regulations."

KPIs this factor influences:

- Defensibility of policies during regulatory exams

- Quality and accuracy of risk assessments

- Credibility of the program in examiners' eyes

- Ability to speak regulator language during exam responses

Experience With Your Institution Type

Compliance requirements and risk profiles differ markedly across institution types. A de novo fintech, a payments processor, and a community bank each face different regulatory expectations, product risks, and examiner relationships. A consultant must understand your specific operating environment.

Operational impact of misaligned experience:

- Time lost educating the consultant on your business model

- Gaps in program design tailored to your risk profile

- Missed regulatory nuances that surface as exam findings

- Policies that don't scale with your product roadmap

- Disconnect between consultant recommendations and operational reality

Ask candidates directly: "Have you worked with organizations like ours? What specific challenges did they face, and how did you address them?"

Proactive Approach and Audit Readiness Focus

The critical distinction is between consultants who react to compliance problems after they materialize versus those who proactively assess risk, track regulatory developments, and maintain programs in an exam-ready state year-round.

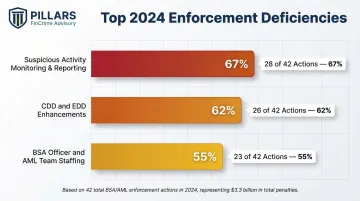

Analysis of 2024 enforcement actions reveals the top deficiencies:

- Suspicious activity monitoring and reporting (cited in 28 of 42 actions)

- CDD and EDD enhancements (cited in 26 of 42 actions)

- BSA officer and AML team staffing (cited in 23 of 42 actions)

A proactive consultant identifies these gaps before regulators do.

KPIs this factor influences:

- Exam outcomes and overall CAMELS ratings

- Number of Matters Requiring Attention (MRAs) or Matters Requiring Immediate Attention (MRIAs) issued

- Time to remediation for identified deficiencies

- Program maturity and sophistication ratings

Scalability of Services

Fintechs and payments companies grow rapidly—transaction volumes expand, new products launch, and regulatory footprints widen. Evaluate whether the consultant's service model can scale alongside your business without requiring a full re-engagement.

Key questions to ask candidates:

- How do you handle increased scope mid-engagement?

- What happens when we launch a new product or enter a new jurisdiction?

- Are your deliverables and workflows designed to grow with the client?

- Can you scale support without rotating teams or losing institutional knowledge?

Look for consultants whose engagement model is structured around your growth trajectory — not just your current state. A fixed-scope retainer that can't flex when you add a new product line creates friction at the worst possible moment.

Communication Style and Engagement Model

Clear, timely communication is operationally critical. Compliance decisions often carry tight regulatory deadlines, and a consultant who is slow to respond or unclear in their guidance creates downstream risk for the institution.

Evaluate these concrete factors:

- What deliverables does the consultant provide (written policies, gap reports, exam prep memos)?

- How frequently do they engage—weekly check-ins, monthly reviews, or ad hoc availability?

- Do they offer a dedicated point of contact or a rotating team structure?

- Can they translate regulatory requirements into plain language for your board and executives?

- How do they handle urgent questions or emerging regulatory developments?

In practice, this means your compliance consultant should be reachable when a regulator inquiry lands on a Friday afternoon — and able to walk your team through a response the same day.

How Pillars FinCrime Advisory Can Help

Pillars FinCrime Advisory is a financial crime compliance partner built specifically for fintechs, payments companies, and financial institutions. Founder Joshua Douglas brings 12+ years in financial crime, nearly 20 years across financial services, and CAMS certification — delivering hands-on expertise when and where you need it.

That experience shapes how Pillars engages with clients. The firm works across the complete compliance lifecycle — from policy development and risk assessments to transaction monitoring optimization and audit readiness — eliminating the coordination friction that comes from managing multiple vendors.

Key differentiators:

- CAMS certification backed by real regulatory exam experience, not just theoretical knowledge

- Data-driven program design that balances compliance requirements with operational efficiency

- Service models built to grow alongside your business — retainer, project-based, or fractional CCO/BSA Officer

- Clients come away with higher alert quality, less operational friction, and greater confidence heading into regulatory exams

Pillars operates nationwide from Houston, Texas, serving clients across the country with flexible engagement models—from project-based work to ongoing fractional CCO/BSA Officer relationships.

Conclusion

Choosing a regulatory compliance consultant is a strategic decision. The goal isn't finding the most recognizable firm, but the one whose FinCrime expertise, engagement model, and scalability align with your organization's specific risk profile and growth trajectory.

Regulatory expectations evolve, business models change, and transaction volumes grow. Your consultant relationship should be designed to adapt continuously—not simply deliver an initial assessment and step away.

Start by conducting an honest internal assessment of your current compliance gaps and program maturity. Identify where you lack depth, where exam findings might surface, and where growth is outpacing your controls. The consultant you choose should be equipped to meet you there — and scale alongside you as the risk landscape shifts.

Frequently Asked Questions

What does a risk and compliance consultant do?

A risk and compliance consultant helps organizations identify, assess, and manage regulatory risk. In the FinCrime context, this includes designing AML/BSA programs, conducting risk assessments, optimizing transaction monitoring, and preparing clients for regulatory exams with defensible documentation and controls.

What are the 5 key principles of compliance?

Five principles define a sound compliance program — each maps directly to financial crime program design expectations:

- Risk-based approach: Tailor controls to your actual risk profile

- Leadership commitment: Board and executive engagement

- Documented policies and procedures: Written, enforceable frameworks

- Training and awareness: Ongoing staff competency

- Monitoring and testing: Independent, periodic validation

What credentials should a financial crime compliance consultant have?

CAMS (Certified Anti-Money Laundering Specialist) is the gold standard credential in FinCrime compliance. Additionally, look for direct regulatory experience, familiarity with BSA/AML obligations, and knowledge of current FinCEN examination priorities. Credentials alone don't guarantee competence, but their absence is a red flag worth taking seriously.

When should a fintech hire a regulatory compliance consultant?

Key trigger points include: launching a new product or entering a regulated market, preparing for a regulatory exam, experiencing rapid growth in transaction volume, or identifying program gaps that internal resources cannot address. Early engagement prevents costly remediation later.

What is the difference between a compliance officer and a compliance consultant?

A compliance officer is an internal employee managing day-to-day program operations, policy implementation, and regulatory reporting. A consultant is an external expert brought in for a defined scope — such as a program build, exam readiness, or gap remediation — then disengaged when the work is complete.