Introduction

Fintech companies face a harsh reality: rapid growth and product innovation collide with escalating regulatory scrutiny around financial crime. Between 2021 and 2025, FinCEN and state regulators levied massive fines against Money Services Businesses (MSBs) and crypto platforms — including Binance's $3.4 billion penalty, BitMEX's $100 million fine, and Block's $40 million NYDFS consent order.

The enforcement pattern is clear: SAR backlogs, transaction monitoring failures, and KYC/CDD gaps trigger consent orders that can derail funding rounds and licensing approvals.

Choosing the wrong fractional FinCrime advisor carries consequences beyond wasted fees — failed regulatory exams, enforcement actions, and audit findings that damage your standing precisely when you need credibility most.

The rise of fractional executives reflects this urgency: requests for interim C-suite placements surged 310% between 2020 and 2024, while 93% of fintechs report struggling to meet compliance requirements. The decision matters. Your advisor must deliver programs that withstand regulatory scrutiny, not generic templates that collapse under examiner review.

Key Takeaways

- The right fractional FinCrime advisor gives you senior compliance expertise on demand — without the overhead of a full-time hire

- Look for fintech-specific regulatory experience, not just general banking compliance background

- Verify CAMS credentials, audit readiness experience, and demonstrated fintech program-building track record

- Red flags include vague compliance experience, no verifiable fintech clients, and inability to discuss BSA/AML specifics

- A structured vetting framework is the difference between a strong compliance hire and a costly misstep for your program and regulatory standing

What Is a Fractional FinCrime Advisor?

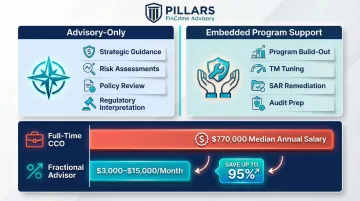

A fractional FinCrime advisor is a senior financial crime compliance professional who works with fintechs on a part-time, retainer, or project basis to build, assess, or optimize anti-financial crime programs—without the overhead of a full-time hire. Full-time Chief Compliance Officers in the technology sector command median total compensation of $770,000. Fractional advisors typically cost $3,000 to $15,000 per month—executive-level expertise without the executive-level overhead.

Fractional FinCrime support comes in two primary forms:

- Advisory-only roles — Strategic guidance, risk assessments, policy review, and regulatory interpretation

- Embedded program support — Hands-on build-out, transaction monitoring tuning, SAR backlog remediation, and audit preparation

Why Fintechs Rely on Fractional FinCrime Expertise

Fintechs face the same BSA/AML, sanctions, and fraud obligations as banks but rarely have the infrastructure to staff a full compliance function from day one.

Regulatory expectations don't scale with company size. FinCEN's MSB registration requirements, state money transmitter licensing obligations, and the 2011 Prepaid Access Rule apply regardless of headcount.

Fractional advisors allow fintechs to access senior-level FinCrime expertise at critical inflection points:

- New product launches requiring compliance program expansion

- Regulatory exams demanding audit-ready documentation

- Rapid scaling that outpaces existing compliance controls

- Sponsor bank onboarding requiring bank-ready programs

Knowing when—and who—to bring in is where the vetting process becomes essential.

What to Look for When Vetting a Fractional FinCrime Advisor

The right fractional FinCrime advisor brings more than credentials—they bring fintech-specific experience that maps directly to your regulatory environment. The factors below connect an advisor's background to the outcomes you actually need: audit-ready programs, scalable policies, and defensible transaction monitoring frameworks.

Fintech-Specific Regulatory Experience

General compliance experience from a large bank does not automatically translate to fintech. Banks operate under different regulatory frameworks, reporting structures, and risk profiles than MSBs, prepaid access providers, or virtual currency platforms.

Verify that the advisor has direct experience navigating:

- FinCEN guidance for MSBs, including 31 CFR Part 1022

- State money transmitter licensing obligations across multiple jurisdictions

- BSA/AML requirements specific to payments and fintech business models

- FinCEN's 2011 Prepaid Access Rule and 2019 Convertible Virtual Currency Guidance

Ask candidates to describe:

- Specific fintech or payments clients they have supported

- The regulatory frameworks those engagements involved

- How they handled MSB registration, SAR filing obligations, or state licensing coordination

If an advisor cannot speak specifically to these frameworks, their experience won't map to your regulatory environment.

Relevant Credentials and Certifications

Credentials signal a baseline of verified expertise. For FinCrime work, the CAMS (Certified Anti-Money Laundering Specialist) designation is the industry benchmark. With over 57,000 certified members globally, CAMS requires 40 eligibility credits and recertification every three years, ensuring practitioners maintain current knowledge.

Look for CAMS as a minimum qualification. Additional relevant certifications include:

- CFCS (Certified Financial Crime Specialist) — Covers 12 core areas of financial crime

- Other specialized certifications — Depending on your specific needs (fraud, sanctions, crypto)

Critical caveat: Certifications alone are not sufficient. They must be paired with demonstrated, hands-on experience applying that knowledge in fintech or payments environments.

Track Record in Financial Crime Program Development

Fintechs often need more than advisory opinions—they need someone who has built or rebuilt financial crime programs from the ground up. This includes policy development, risk assessments, transaction monitoring design, and SAR workflow optimization.

Ask the advisor to walk through a specific program they built or significantly improved:

- What did the program look like before their involvement?

- What specific changes did they implement?

- What measurable outcomes resulted—improved alert quality, reduced false positives, cleaner exam findings?

If an advisor cannot provide concrete examples with verifiable outcomes, they may lack the hands-on experience your fintech requires.

Audit Readiness and Regulatory Exam Experience

The ultimate test of a FinCrime program is how it holds up under regulatory scrutiny. An advisor who has supported fintech clients through actual examinations or audits brings practical knowledge that no amount of theoretical expertise can replicate.

FinCEN delegates MSB examination authority to the IRS, which conducts reviews using the FFIEC BSA/AML Examination Manual and the MSB Examination Manual. State regulators require MSBs to be examined at least every 60 months, with initial exams often occurring within 24 months of licensure.

For nationwide payments firms operating in 40+ states, the CSBS "One Company, One Exam" program allows a single comprehensive exam to satisfy multiple state requirements simultaneously.

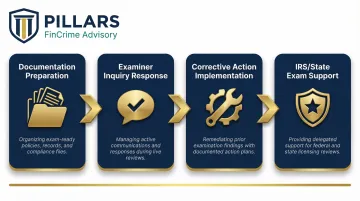

Look for evidence of:

- Experience preparing exam-ready documentation

- Responding to examiner inquiries during active reviews

- Implementing corrective actions from prior findings

- Supporting clients through IRS-delegated exams or state licensing reviews

Exam experience isn't just about passing—it's about knowing which documentation gaps examiners flag, how to respond under pressure, and what corrective actions actually satisfy regulators. That comes from direct exposure, not preparation guides.

Scalability Mindset

Fintechs don't just need a program that works today—they need one built to scale as the business grows, adds new products, or enters new markets. The advisor should demonstrate experience designing programs that are flexible and can absorb growth without requiring a full rebuild.

Probe for specific examples of how the advisor has:

- Structured policies to accommodate volume growth or product expansion

- Designed transaction monitoring thresholds that scale without triggering operational breakdowns

- Built risk assessment frameworks that adapt to new business lines

- Created documentation that withstands audit scrutiny at multiple stages of growth

Your advisor should know the difference between compliance infrastructure that passes today's exam and infrastructure that still holds up when transaction volume doubles and you've entered three new states.

Engagement Model and Communication Approach

The structure of the engagement matters. Understand whether the advisor works on a retainer, project basis, or hourly model, and whether their availability aligns with your needs—particularly during exam cycles or product launches when responsiveness is critical.

Evaluate during the vetting process:

- Can they explain complex regulatory concepts in plain language?

- Do they ask diagnostic questions about your specific business model?

- Do they demonstrate collaborative partnership, not distant consulting?

- Can they commit to availability during critical periods?

A strong fractional advisor functions as an embedded partner, not an occasional consultant who responds to emails when convenient.

Red Flags That Should End the Conversation

End the conversation if an advisor:

- Cites only bank or insurance compliance experience without speaking specifically to FinCEN's expectations for MSBs, prepaid access rules, or virtual currency guidance

- Cannot provide references from fintech or payments company clients, or responds with vague answers when asked for verifiable relationships

- Leads with deliverable templates or canned policy frameworks rather than beginning with a diagnostic assessment of your specific risk environment

Each of these patterns points to the same underlying problem: an advisor selling speed over fit. Examiners look for evidence that controls are tailored to your actual business model — generic policies don't satisfy that standard. If an advisor offers "turnkey" solutions before understanding your risk profile, what they're delivering is compliance theater.

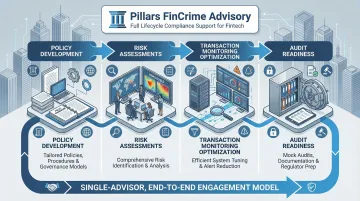

How Pillars FinCrime Advisory Can Help

Pillars FinCrime Advisory checks the boxes this guide outlines: deep domain expertise, scalable program design, and a single accountable advisor across the full compliance lifecycle. Founded by Joshua Douglas, a CAMS-certified professional with 12+ years in financial crime and nearly 20 years across financial services, Pillars offers full lifecycle financial crime program support—from policy development and risk assessments through transaction monitoring optimization and audit readiness.

Key differentiators that make Pillars the right partner for fintechs evaluating fractional FinCrime advisory support:

- Tailored, data-driven solutions — Every engagement is built around your specific business model and risk profile, not recycled compliance templates

- Programs built to be scalable and audit-ready — Fintechs are prepared for regulatory exams at any stage of growth

- End-to-end support from a single, experienced advisor — Eliminates the coordination overhead of managing multiple consultants across different compliance functions

Michael Thompson, VP of Compliance Operations, reported measurable improvements in alert quality, reduced operational friction, and stronger regulatory exam readiness after Pillars completed transaction monitoring optimization and KYC redesign work.

James Donovan, Chief Compliance Officer, noted that Pillars helped his team navigate a complex regulatory review—leaving them with a program that is now scalable and audit-ready.

For fintechs seeking fractional FinCrime advisory support that meets the vetting criteria outlined in this guide, contact Pillars FinCrime Advisory at 281-825-1603 or pillarsfincrimeadvisory@gmail.com.

Conclusion

Vetting a fractional FinCrime advisor is not a checkbox exercise—it is a high-stakes decision that directly affects your regulatory standing, your program's defensibility, and your ability to scale with confidence. The enforcement wave targeting fintechs and MSBs makes this clear: inadequate compliance programs carry material consequences, including consent orders, civil money penalties, and damaged relationships with sponsor banks and investors.

The right fractional advisor clears a high bar. Use these criteria as your baseline every time you evaluate a candidate:

- Fintech-specific expertise in AML, KYC/KYB, and payments risk — not general compliance experience

- Verifiable credentials (CAMS or equivalent) with a track record of audit-ready program builds

- Demonstrated experience navigating regulatory exams and sponsor bank relationships

- An engagement model that fits your stage, budget, and operational pace

Revisit the fit as your program evolves. Advisors who excel at building foundational programs don't always have the depth to manage a complex, scaled operation — and your vetting process should reflect that. Choose advisors who have proven they can deliver programs that withstand regulatory scrutiny.

Frequently Asked Questions

What is the difference between a fractional FinCrime advisor and a full-time compliance officer?

A fractional advisor delivers senior-level financial crime expertise on a part-time or project basis—without the $770,000 median total compensation of a full-time CCO. It's a cost-effective model for fintechs that need strategic guidance or program support at a fraction of the cost.

What credentials should a fractional FinCrime advisor have?

The CAMS designation is the primary industry benchmark for AML expertise. CFCS or other certifications may also be relevant depending on scope. Credentials matter, but hands-on experience in fintech or payments environments is equally important. A certification shows baseline knowledge; a track record shows what an advisor can actually do.

When should a fintech hire a fractional FinCrime advisor instead of building in-house compliance staff?

Fractional support makes the most sense when you need immediate senior-level expertise—ahead of a regulatory exam, during a product launch, or when building a compliance program from scratch—before your scale justifies a full-time hire.

How much does a fractional FinCrime advisor typically cost?

Fractional executives typically cost $3,000–$15,000 per month or $175–$450 per hour, depending on scope, engagement model (retainer vs. project), and experience level. Both options are significantly less than the $770,000 median total compensation for a full-time technology sector CCO.

What questions should I ask a fractional FinCrime advisor during the vetting process?

Ask about specific fintech clients and regulatory frameworks they have worked with, how they have handled regulatory exams, and how they approach building scalable, audit-ready compliance programs tailored to your specific business model. Request concrete examples with measurable outcomes.

How do I know if my fintech's compliance program actually needs outside advisory support?

Common indicators include upcoming regulatory exams with no internal exam readiness process, transaction monitoring alert quality issues, policy gaps flagged in audits, or a team stretched too thin to maintain program documentation. Any of these signal that fractional FinCrime advisory support could provide material value.