Introduction

AI tools are now embedded in the core of financial crime compliance — transaction monitoring, fraud detection, customer risk scoring. That's not a future state; it's the present reality for most fintechs, payments companies, and financial institutions.

The problem is that the same AI systems improving operational efficiency are creating new regulatory exposure. Regulators aren't just asking whether you use AI. They're asking how it works, why it made a specific decision, whether it's fair, and whether you can prove it in an exam.

Many organizations can't answer those questions confidently. The governance infrastructure hasn't kept pace with the technology deployment.

This article covers:

- What AI regulatory compliance actually means in financial crime contexts

- The specific risks of deploying AI in AML and fraud programs

- The evolving regulatory landscape, including the EU AI Act and FinCEN's proposed rule

- A practical framework for building AI governance that holds up under scrutiny

Key Takeaways

- AI regulatory compliance means ensuring AI systems satisfy both existing financial regulations and emerging AI-specific rules, not just performance benchmarks

- The four biggest risks: algorithmic bias, "black box" decision-making, data privacy gaps, and missing audit trails

- FinCEN's 2026 proposed AML/CFT rule explicitly references AI and machine learning as part of effective program evaluation

- The EU AI Act carries fines up to €35 million or 7% of global turnover for the most serious violations

- Building an AI-ready compliance framework requires expert advisory guidance, not just better software

What Is AI Regulatory Compliance?

AI regulatory compliance means the decisions, policies, and controls that ensure an organization's AI systems are developed and deployed in line with applicable laws, regulations, and internal governance standards. It goes beyond legal checkboxes to encompass fairness, transparency, and accountability in how AI makes or influences decisions.

For fintechs, payments companies, and financial institutions, that definition carries real stakes. AI systems in these organizations directly influence high-consequence decisions:

- Which transactions get flagged for investigation

- Which customers receive fraud alerts or account restrictions

- Which counterparties pass KYC/KYB review

Regulatory scrutiny and consumer harm risk are highest precisely where AI is most active.

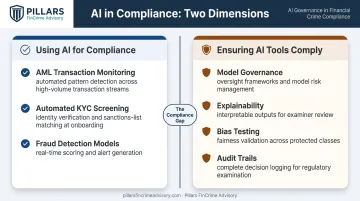

The Dual Compliance Problem

There are two compliance dimensions that often get conflated — a conflation that creates real program gaps:

- Using AI to meet compliance obligations — AI-powered AML monitoring, automated KYC screening, fraud detection models

- Ensuring those AI tools themselves comply with applicable rules — model governance, explainability, bias testing, audit trails

Most organizations focus heavily on the first dimension. The second is where regulators are now focusing their attention, and where many compliance programs have meaningful gaps to close.

How AI Is Reshaping Financial Crime Compliance

AI is changing the mechanics of financial crime compliance in three meaningful ways: how institutions monitor transactions, how they manage third-party risk, and how they track regulatory change.

AML and Transaction Monitoring

Traditional rule-based transaction monitoring works on fixed thresholds and static scenarios. The problem is that financial crime patterns evolve faster than rule sets get updated, producing high volumes of low-quality alerts.

AI-driven monitoring learns from transaction data to identify subtle, evolving patterns — improving alert quality and enabling more targeted risk prioritization. McKinsey's research on machine learning in AML found that replacing rule-based tools with ML at leading financial institutions produced efficiency gains of up to 30% and improved suspicious-activity identification by up to 40%.

The regulatory context is shifting to match. FinCEN's April 2026 proposed rule on AML/CFT programs explicitly states that program effectiveness evaluation may consider whether institutions are employing innovative tools such as artificial intelligence and machine learning. The proposed effective date would be 12 months after a final rule is issued.

Third-Party Risk Management

For fintechs and payments companies with complex vendor networks, periodic manual reviews leave meaningful gaps. AI tools close those gaps by continuously scanning:

- Financial reports and regulatory filings for early warning indicators

- Adverse news feeds for reputational and sanctions exposure

- Sanctions lists and watchlists in real time

The capability shift is real, but it introduces governance questions about how AI outputs are interpreted, escalated, and documented — questions compliance programs need to address before deployment, not after.

Regulatory Change Management

Keeping pace with FinCEN, CFPB, and state regulators simultaneously is one of the more underestimated operational burdens in compliance. AI systems help by scanning regulatory publications as they're released, categorizing changes by impact area, and surfacing what needs immediate attention. The practical result is a shorter lag between a new requirement and program adaptation — which matters when multiple agencies are active at the same time.

Key Compliance Challenges When Deploying AI in Financial Services

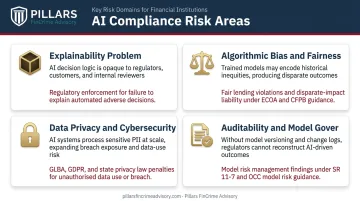

AI deployment in financial crime programs doesn't just create efficiency — it creates new compliance exposure. Four risk areas consistently surface when regulators examine AI-driven AML and fraud detection systems.

The Explainability Problem

Most U.S. banking regulators expect firms to explain why a specific decision or alert was generated. Many machine learning models — particularly ensemble and deep learning models — operate as "black boxes" that can't produce that explanation in a form that satisfies an examiner.

The CFPB made its position clear: algorithmic complexity is not an excuse for noncompliance with adverse action notice requirements under ECOA and Regulation B. OCC Acting Comptroller Michael Hsu's 2024 speech similarly identified the black-box nature of AI as an accountability challenge requiring controls commensurate with model complexity.

During an exam, an examiner who asks "why did your system generate this SAR?" needs a documented, defensible answer — not a confidence score.

Algorithmic Bias and Fairness Risk

AI models trained on historical transaction data can encode existing disparities. The result: disproportionate flagging of transactions from certain demographics or geographies — patterns that look like model behavior rather than intentional discrimination, but that carry the same regulatory and reputational exposure.

Regulators have drawn a hard line here. A 2023 joint statement from the CFPB, DOJ Civil Rights Division, EEOC, and FTC explicitly warned that automated systems can produce unlawful discrimination under existing civil rights and fair lending laws — regardless of intent. Colorado's AI Act (SB24-205) goes further, requiring developers and deployers of high-risk AI systems — including those used in financial and lending decisions — to take reasonable care to protect consumers from algorithmic discrimination.

Data Privacy and Cybersecurity Exposure

AI compliance tools require access to large volumes of sensitive customer and transaction data. That creates a larger attack surface. Compliance teams need to ensure AI systems are architected in line with:

- GLBA / FTC Safeguards Rule — requires written information security programs, access controls, encryption, and service-provider oversight; the 2021 amended rule extended these requirements with more specificity

- State privacy laws — Colorado Privacy Act (effective July 2023), Virginia CDPA, and California CCPA/CPRA each create consumer rights around profiling and data use

- NYDFS guidance — NYDFS's October 2024 Industry Letter specifically addresses cybersecurity risks arising from AI, including exposure of nonpublic information

Deploying AI for analytical efficiency without addressing these architectural requirements is a compliance failure — one examiners are increasingly equipped to identify.

Auditability and Model Governance Gaps

AI models that learn and adapt over time may behave differently at examination than when they were originally validated. Federal Reserve SR 11-7 — the longstanding model risk management guidance — defines a model broadly enough to encompass AI and ML systems used in AML and fraud detection, meaning banks face documentation requirements covering model inputs, logic, and performance metrics.

Many fintech compliance teams haven't operationalized this. The governance gap typically surfaces when regulators request model validation records and what exists is either sparse or outdated.

Third-party vendor risk compounds the problem. Many fintechs rely on external vendors for AI-powered compliance tools, but if the vendor's model is biased, opaque, or non-compliant, the financial institution remains accountable — not the vendor. Due diligence and ongoing performance monitoring of third-party AI tools is a compliance obligation, not a procurement consideration.

The Evolving AI Regulatory Landscape

There is no single comprehensive AI law in the U.S. What exists is a patchwork of sector-specific financial regulations, emerging federal guidance, and increasingly active state legislation — all of which apply to AI outputs and decisions in financial services.

That U.S. fragmentation doesn't insulate fintechs from international exposure. For firms serving EU customers, the EU AI Act creates direct compliance obligations — regardless of where the company is headquartered.

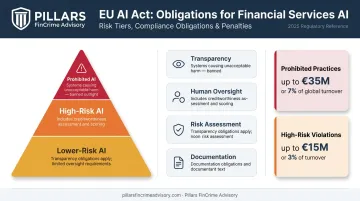

The EU AI Act and Its Extraterritorial Reach

The EU AI Act (Regulation 2024/1689) is the first comprehensive AI regulatory framework globally. It entered into force August 1, 2024, with phased implementation through 2027.

Key points for U.S.-based fintechs:

- Extraterritorial scope: The Act applies to providers in third countries where AI system outputs are used in the EU — meaning U.S. fintechs serving EU customers may fall within scope

- High-risk classification: AI systems used to evaluate creditworthiness or establish credit scores fall under Annex III high-risk categories; fraud detection AI is expressly carved out from that specific category, but compliance teams should assess each use case

- Compliance obligations: Transparency requirements, human oversight, risk assessments, and documentation for high-risk systems

- Penalties: Up to €35 million or 7% of global turnover for prohibited AI practices; up to €15 million or 3% of turnover for most other high-risk AI obligation violations

U.S. Regulatory Expectations for AI in Financial Crime Programs

The U.S. approach remains fragmented, but that doesn't mean compliance teams can afford to wait for a unified AI law.

Current regulatory touchpoints include:

| Source | Relevance |

|---|---|

| FinCEN 2026 AML/CFT NPRM | Explicitly references AI/ML as part of effective program design |

| SR 11-7 / OCC 2011-12 | Model risk management framework applies to AI/ML systems meeting the model definition |

| CFPB ECOA/Reg B guidance | Algorithmic explainability required for adverse action notices |

| 2023 joint agency AI statement | Existing civil rights and fair lending laws apply to AI outputs |

| Treasury March 2024 report | Addresses AI-specific cybersecurity and operational risks in financial services |

At the state level, two jurisdictions have moved furthest with direct AI obligations:

- Colorado AI Act: Covers high-risk AI used in financial and lending decisions, with requirements for impact assessments and consumer disclosures

- NYDFS cybersecurity guidance: Addresses AI-specific risks for regulated entities, including third-party AI system exposure

For multi-state fintechs and payments companies, the practical challenge is policy versioning — maintaining compliance across jurisdictions with different thresholds, disclosure requirements, and enforcement timelines. A regulatory change management process isn't optional at this point; it's a program design requirement.

Building an AI-Ready Compliance Framework

Governance comes first. Technology deployment without the underlying documentation, oversight, and policy infrastructure creates the conditions for a regulatory problem.

Step 1: Build an AI Use Inventory

Document every AI tool used in your compliance program — what decisions it influences, what data it processes, what human oversight checkpoints exist. This is the baseline for both internal governance and examiner readiness. Without it, you can't demonstrate control over your own program.

Step 2: Implement Model Governance

In practice, this means:

- Validation before deployment (not after)

- Periodic performance reviews on defined schedules

- Clear escalation protocols when AI output is questioned or anomalous

- Maintained documentation that can survive an exam or enforcement inquiry

Step 3: Keep Humans in the Loop

AI should augment compliance judgment, not replace it. Regulators expect human review and accountability for final compliance decisions — particularly in AML and fraud contexts. Staffing models and alert review workflows need to be designed with this expectation built in. A high-quality AI model that routes every decision to automated disposition without human review is still a regulatory liability.

Step 4: Close Policy and Training Gaps

AI deployment must be supported by:

- Updated internal policies governing AI use and bias testing protocols

- Staff training so compliance teams can interpret, challenge, and document AI-generated outputs

- Clear escalation paths when AI outputs conflict with analyst judgment

Staff who can't explain how an AI system reached a conclusion can't document that decision for an examiner. Training isn't optional in an AI-enabled compliance program.

Pillars FinCrime Advisory helps fintechs and financial institutions build this governance infrastructure and audit-ready documentation before regulators arrive — treating it as a deliberate program investment, not a reactive fix.

Frequently Asked Questions

What is AI regulatory compliance?

AI regulatory compliance refers to the policies, controls, and practices ensuring an organization's AI systems are deployed in line with applicable laws, regulations, and governance standards. It covers fairness, transparency, auditability, and data privacy — not just whether a system technically functions within legal limits.

How does the EU AI Act affect U.S. financial institutions?

The EU AI Act has extraterritorial reach: it applies when AI outputs are used in the EU, regardless of where the provider is based. U.S. fintechs serving EU customers may face transparency, human oversight, and risk assessment obligations for AI systems that qualify as high-risk under the Act.

What are the biggest risks of using AI in AML compliance programs?

The primary risks include algorithmic bias, black-box models that examiners can't evaluate, data privacy vulnerabilities from large sensitive datasets, and over-reliance on AI without human oversight. Any of these can trigger regulatory sanctions.

Do regulators require AI tools used in compliance programs to be explainable?

Yes. U.S. banking regulators expect firms to document and explain AI-driven compliance decisions — SR 11-7 model risk management principles apply directly to AI/ML systems. The CFPB has also confirmed that algorithmic complexity doesn't excuse noncompliance with adverse action notice requirements.

How can fintechs manage third-party AI vendor compliance risk?

Firms remain accountable for vendor compliance failures. Robust due diligence, contractual protections, and ongoing model performance monitoring are essential to prevent third-party AI tools from introducing undetected bias or opacity into your compliance program.

Can AI replace human compliance officers in financial institutions?

No. AI is effective at processing data, detecting patterns, and automating routine tasks, but regulators expect human accountability for compliance decisions — especially in AML and fraud. Human expertise and oversight aren't optional features; they're regulatory expectations.