Introduction

According to McKinsey, up to 90% of alerts in rule-based AML transaction monitoring systems are false positives. A separate McKinsey report puts it even more starkly: customer-risk rating and transaction monitoring models "often exhibit false positive rates of over 98 percent."

For most compliance teams, that means analysts spend the bulk of their day clearing alerts that will never produce a SAR — work that generates cost without generating results.

The problem runs deeper than operational waste. Tightening thresholds to cut alert volume risks missing genuine financial crime, and regulators treat that failure far more seriously than a false positive problem. Left unaddressed, alert backlogs grow, SAR deadlines slip, and high-value customers leave after their legitimate transactions are repeatedly delayed or questioned.

This guide covers what AML false positives actually are, why traditional systems generate so many of them, what they cost, how to calculate your rate, and six proven strategies for reducing them — while keeping your program defensible during exams.

Key Takeaways

- Static, poorly tuned rules with uniform thresholds are the primary driver of false positives

- Industry false positive rates commonly exceed 90%, representing a substantial operational and financial burden

- False positives and false negatives are opposite failure modes — both carry serious consequences

- Sustainable reduction depends on better data, risk-based segmentation, and calibrated monitoring — not one-time fixes

- Ongoing governance and audit-ready documentation are non-negotiable for exam defensibility

What Are AML False Positives?

A false positive in AML is an alert generated by a transaction monitoring or sanctions screening system that flags a legitimate customer transaction or entity as suspicious — only for investigation to confirm no actual wrongdoing occurred. The opposite, a true positive, is a genuine suspicious activity alert that warrants escalation or a SAR filing.

Two Examples That Resonate

Example 1 — Seasonal business volume spike: A landscaping company processes three times its typical monthly transaction volume during spring. A rule-based system flags the spike as potential structuring or unusual activity. The investigator clears it in five minutes. The system alerts again next spring.

Example 2 — The $9,800 deposit: A customer deposits $9,800 in legitimate proceeds. Because the amount falls just below the $10,000 CTR reporting threshold, a rule flags it as potential structuring. The customer's history shows similar deposits every payday. The alert is closed as non-suspicious — for the third time this quarter.

Both patterns look suspicious to a rule that evaluates dollar amounts without context. Neither represents financial crime.

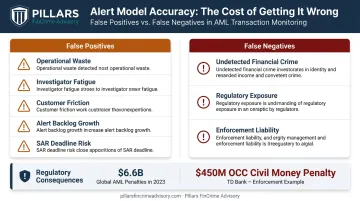

False Positives vs. False Negatives

These two failure modes pull in opposite directions:

- False positives — legitimate activity flagged as suspicious, creating operational waste and investigator fatigue

- False negatives — genuine suspicious activity that passes through undetected, creating direct regulatory exposure

Fenergo reported $6.6 billion in global AML, KYC, sanctions, and CDD penalties in 2023 — a 57% surge from the prior year. TD Bank's 2024 FinCEN consent order cited more than 70,000 backlogged detection alerts that delayed notification of suspicious activity to law enforcement, contributing to a $450M OCC civil money penalty.

Those numbers illustrate why reducing false positives and managing false negative risk must happen together. Lowering system sensitivity to cut alert volume can inadvertently let genuine threats slip through — and that's where programs draw regulatory scrutiny. The goal isn't fewer alerts; it's better ones.

Why AML Systems Generate So Many False Positives

Static Rules Without Context

Most legacy transaction monitoring systems run on uniform, static thresholds applied across an entire customer population. A rule that flags all transactions over $X catches a commercial real estate firm's routine wire transfers as often as it catches actual structuring attempts. The rule has no mechanism to distinguish between them.

The FFIEC BSA/AML Examination Manual directly addresses this: thresholds should enable detection of unusual activity consistent with the institution's risk profile, and filtering criteria should be independently reviewed for reasonableness. Static, uncalibrated rules don't meet that standard.

No Contextual Awareness

Traditional systems evaluate transactions in isolation. A $200,000 wire transfer reads very differently for an established commercial real estate firm than for a retail account opened six weeks ago — but a rule-based system treating both the same will alert on both.

Without visibility into a customer's occupation, typical business activity, transaction history, or account purpose, the monitoring engine has no baseline for "normal." Any transaction outside the rule's narrow band triggers an alert.

Data Quality Gaps

When customer records are outdated, inconsistently formatted, or siloed across systems, the monitoring engine works from an incomplete picture. Missing or inaccurate business type data means a wholesale distributor gets treated like a retail consumer. That mismatch drives alert volumes up without improving detection quality.

Sanctions Screening Name Matching

The FCA has specifically documented how sanctions screening systems struggle with name formats that don't map cleanly to watchlist entries. Common triggers include:

- Non-Latin characters and variant transliterations

- Honorifics and name prefixes

- One-word names or names containing digits

- Names exceeding system character limits

Each generates a partial match requiring manual review — even when no actual sanctions hit exists.

Regulatory Over-Correction

Institutions facing enforcement pressure often deliberately widen their alert nets, preferring to over-alert rather than risk missing a genuine threat. FinCEN's outreach guidance to large depository institutions warns that over-focusing on rules and scenarios can divert attention from system performance, false positive analysis, and other configurations that affect overall effectiveness. A high false positive rate signals a miscalibrated system, not a cautious one.

The Real Cost of High False Positive Rates

Compliance Cost at Scale

LexisNexis Risk Solutions data shows financial crime compliance costs reached $61 billion in the U.S. and Canada alone, with 99% of financial institutions reporting increased costs. EMEA costs reached $85 billion. APAC compliance costs are approaching $45 billion. These figures reflect labor, technology, and operational overhead — much of which is consumed by alert investigation activity.

Customer Experience Damage

Legitimate customers whose transactions are held, questioned, or declined experience real friction. Business customers who depend on timely payment processing are particularly affected. Chronic over-alerting leads to account attrition — the customers most likely to leave are often the highest-value ones, who have the most options.

The FCA has documented cases where payment delays caused by screening backlogs left funds unavailable for months, affecting customers' ability to receive salary, operate businesses, and meet basic financial obligations.

The Examiner Risk Most Teams Overlook

Alert backlogs created by excessive false positives can push SAR filing past regulatory deadlines. FinCEN requires SARs to be filed no later than 30 calendar days after initial detection of suspicious activity; the outer limit with an unidentified suspect is 60 days. When analysts are buried in false positive reviews, genuine alerts can age past those deadlines. That creates a compliance failure even when the suspicious activity is eventually identified.

Examiners don't only look at whether monitoring is in place — they scrutinize how alert processes are managed day to day. Common exam findings in over-burdened programs include:

- Alert backlogs with no documented remediation plan

- SARs filed past the 30-day (or 60-day) deadline

- Disposition documentation that can't support examiner review

How to Calculate Your AML False Positive Rate

The standard operational formula is:

False Positive Rate (%) = [False Positives ÷ Total Alerts Reviewed] × 100

- False positives: Alerts that investigation confirmed were legitimate transactions

- Total alerts reviewed: All alerts dispositioned during the period

Worked example: A monitoring system generates 500 alerts in a month. Investigators clear 460 as non-suspicious. False positive rate = 460 ÷ 500 × 100 = 92%.

No regulator publishes a target rate. Regulators focus on risk-based calibration, threshold documentation, and validation — not a universal benchmark.

McKinsey's research offers useful directional context: advanced statistical modeling can bring false positive rates from above 90% to below 50%, and machine learning can reduce false reports by 20–30%. Leading institutions use those ranges as internal performance targets, not regulatory requirements.

Track your false positive rate as a KPI across three dimensions:

- By rule — identify which scenarios generate the most noise

- By customer segment — surface population-level calibration gaps

- Over time — trends matter more than any single month's number

Proven Strategies to Reduce AML False Positives

Strategy 1: Risk-Based Customer Segmentation

Applying uniform thresholds across an entire customer population is the single largest driver of unnecessary alerts. Segmenting customers by occupation, business type, transaction history, geographic exposure, and PEP status allows tighter thresholds for genuinely high-risk profiles and appropriately calibrated thresholds for lower-risk customers.

McKinsey's research found that advanced analytics applied to segmented populations can reduce incorrectly labeled high-risk customers by 25–50%. The detection improvement is real — and so is the alert volume reduction.

Strategy 2: Improve Data Quality Before Tuning Thresholds

No amount of threshold adjustment compensates for bad underlying data. Structured, standardized customer data — separate fields for name components, validated identifiers, standardized address formats — improves match precision in both transaction monitoring and sanctions screening.

A data quality assessment at program intake should come before any threshold tuning exercise. Tuning thresholds against inaccurate data produces inaccurate results.

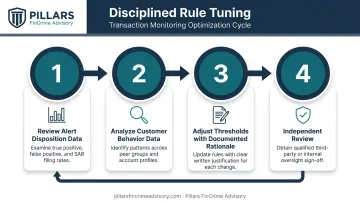

Strategy 3: Systematic Rule Tuning with Documented Rationale

Effective TM optimization follows a disciplined cycle:

- Review alert disposition data — identify which specific rules generate the highest false positive volumes

- Analyze customer behavior data — understand what actual transaction patterns look like for the flagged population

- Adjust thresholds with documented rationale — every change should have a written business reason tied to risk-based logic

- Independent review — FFIEC expects programming and filtering criteria to be independently reviewed for reasonableness

The documentation matters as much as the tuning. Examiners want to see that threshold changes reflect deliberate, risk-based decisions — not reactive adjustments made to reduce workload.

Strategy 4: Behavioral Baselines and Dynamic Monitoring

Static thresholds alert on absolute dollar amounts. Behavioral baseline systems alert on deviations from what's normal for a specific customer or segment. A $50,000 transfer that's routine for one customer looks very different from a $50,000 transfer that's ten times anything a second customer has ever processed.

Modern platforms using machine learning can establish and continuously update these baselines, improving suspicious activity identification by up to 40% and operational efficiency by up to 30%, according to McKinsey's analysis of ML-enhanced AML programs.

Strategy 5: Investigator Feedback Loops

Every alert disposition decision is data. Capturing why an alert was cleared or escalated — at the rule level, with the analyst's reasoning — creates a foundation for continuous improvement. Institutions that systematically route disposition outcomes back into rule refinement cycles see compounding reductions in false positive rates over time.

The feedback loop doesn't require sophisticated technology. It requires a structured disposition workflow that captures more than a binary cleared/escalated outcome.

Strategy 6: Engage Qualified Advisory Support

Many fintechs and growing payments companies lack the internal expertise to conduct a TM optimization review that will hold up under examiner scrutiny. The analysis, threshold change documentation, and model validation evidence all need to be prepared with regulatory expectations in mind from the start — not retrofitted after the fact.

Pillars FinCrime Advisory works directly with fintechs, payments companies, and financial institutions on transaction monitoring optimization and exam readiness. Led by CAMS-certified practitioner Joshua Douglas — 12+ years in financial crime, nearly 20 years across financial services — the firm has helped clients reduce alert volumes, sharpen detection quality, and walk into regulatory exams with documentation that holds up.

Building a Sustainable False Positive Management Program

Why This Is a Program Discipline, Not a Project

An institution that tunes its monitoring system once and moves on will see false positive rates drift upward as its customer mix, product set, and the financial crime typology landscape all evolve. A sustainable program requires:

- Scheduled rule review cycles with defined frequency (quarterly or semi-annual for high-volume systems)

- Clear internal ownership — someone accountable for monitoring system performance, not just alert investigation

- Documented change management — a log of every threshold adjustment, with rationale and approval

The governance structure matters because regulators and examiners increasingly evaluate how institutions manage their alert processes, not just whether monitoring exists.

Audit-Readiness Documentation

Examiners reviewing a transaction monitoring program will look for:

- Tuning rationale memos — written justification for threshold settings and any changes made

- Alert disposition statistics — false positive rate trends by rule and by period

- Rule change logs — a record of what changed, when, why, and who approved it

- Model validation evidence — documentation that the system's performance has been independently assessed

The 2021 interagency statement on model risk management for BSA/AML compliance systems confirmed that AML surveillance and automated transaction monitoring systems are subject to model risk management expectations. That means validation isn't optional for institutions using these systems.

Scaling Compliance Without Scaling Headcount

Fintech and payments companies in growth phases face a compounding problem: as transaction volumes increase, alert volumes grow in step — often outpacing the compliance team's capacity to investigate them. Improving alert quality lets existing capacity cover more ground without adding headcount.

Better alert quality typically delivers three things for scaling organizations:

- Fewer low-value alerts consuming analyst time

- Clearer prioritization of genuinely suspicious activity

- A monitoring program that holds up under examiner scrutiny as volume grows

Pillars FinCrime Advisory works with fintechs and payments companies at exactly this inflection point — building transaction monitoring programs that maintain alert quality through growth, without requiring a large internal compliance team to sustain them.

Frequently Asked Questions

What are false positives in AML?

False positives are alerts generated by AML transaction monitoring or sanctions screening systems that flag legitimate customer activity as suspicious. When investigators review them, no actual wrongdoing is found — the alert represented a legitimate transaction that resembled a suspicious pattern to the detection system.

How do you reduce false positives in AML?

Reduction depends on five core levers: risk-based customer segmentation, data quality improvement, disciplined rule tuning, behavioral baseline monitoring, and investigator feedback loops. Sustainable results require ongoing governance — not a one-time remediation effort.

What is the AML false positive rate?

The false positive rate is the percentage of alerts that investigation confirms were legitimate, calculated by dividing false positive alerts by total alerts reviewed. In traditional rule-based systems, industry rates exceed 90%. Leading institutions target significantly lower rates through risk-based calibration and modern detection logic.

What is false positive reduction?

False positive reduction is the ongoing process of improving AML monitoring precision so compliance teams spend more investigation capacity on genuine threats. It encompasses better data quality, calibrated thresholds, risk-based rules, and modern detection technology.

What is the difference between a false positive and a false negative in AML?

A false positive is a legitimate transaction incorrectly flagged as suspicious, causing operational waste and customer friction. A false negative is genuine suspicious activity that passes through the system undetected, creating regulatory exposure and potential enforcement liability.

Can AML false positives be completely eliminated?

No. Any system sensitive enough to detect sophisticated financial crime will inevitably flag some legitimate activity that resembles suspicious patterns. The goal is reducing false positives to a manageable, risk-justified level while maintaining strong detection effectiveness.