Introduction

Building a compliant AML program sounds straightforward until you realize that a newly licensed payments company and an established fintech processing millions of transactions monthly face completely different problems — even when they're both evaluating the same AI tools.

Regulators don't scale their expectations with company size. Under 31 CFR 1022.210, every money services business must maintain an effective written AML program, and "effective" is judged against the risks the organization actually presents. A startup with modest volume isn't exempt — it just has a narrower risk surface to document and defend.

That risk surface determines the consulting approach. Startups need foundational infrastructure built correctly from day one. Mid-market companies need their existing programs diagnosed, tuned, and scaled. Applying the wrong model to either creates exactly the kind of program gaps that attract regulatory scrutiny.

The enforcement record makes clear what that scrutiny costs. FinCEN's 2022 action against Bittrex resulted in a $29.28 million civil money penalty for BSA violations. This guide helps you identify which consulting approach your organization actually needs — and why the distinction matters before you engage anyone.

Key Takeaways

- Startup AI consulting centers on building a compliant, scalable program before transaction volume outpaces controls.

- For mid-market firms, consulting targets operational friction — false positives, alert backlogs, weak SAR quality — and resolves it without breaking regulatory continuity.

- People and process must be built alongside the technology; AI layered onto a weak compliance foundation creates more risk, not less.

- Choosing the wrong consulting model risks more than budget: it invites remediation under active regulatory scrutiny.

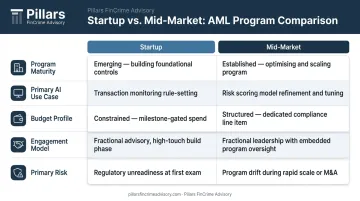

Startups vs. Mid-Market AI Consulting: Quick Comparison

Startup and mid-market engagements look different on paper — and they should. The underlying compliance gaps, resource constraints, and regulatory exposure vary enough that a consulting approach built for one rarely fits the other.

| Dimension | Startup | Mid-Market |

|---|---|---|

| Program maturity | Early or no existing program | Existing program with gaps or scaling stress |

| Primary AI use case | Transaction monitoring setup, customer risk scoring, KYC workflows | Monitoring model tuning, alert quality improvement, risk segmentation |

| Budget profile | Limited; prioritize foundational spend | Moderate to significant; focused on ROI from optimization |

| Engagement model | Project-based or advisory retainer | Embedded advisory or ongoing retainer |

| Primary risk | Building on a weak foundation | Scaling without validating what exists |

Matching the engagement model to current program maturity — not projected growth — is what separates effective advisory work from expensive misalignment. A startup that skips foundational controls to chase optimization tools will hit the same regulatory wall eventually, just with more technical debt attached.

AI Consulting for Startups: Building Compliance Programs from Scratch

The Startup Reality in Financial Services

Early-stage fintechs and payments companies typically operate with lean teams, limited compliance infrastructure, and real regulatory obligations from day one. The size of the transaction volume doesn't change the obligation — it calibrates the risk assessment, not the requirement to have one.

The most common mistake: purchasing AI-enabled transaction monitoring software before establishing the program foundations that make the software usable. FATF's research found that 45% of respondents cited data quality as a primary obstacle to adopting technology-based AML solutions. At the startup stage, data quality problems are the rule, not the exception.

Bolting AI onto a weak compliance foundation produces:

- Alert volumes that overwhelm a small team with no disposition workflow

- SAR narratives that don't meet FFIEC quality standards

- Transaction monitoring logic that hasn't been calibrated to the company's actual business model

- Exam findings that treat the AI tool as a governance failure, not a technology win

What Startup AI Consulting Should Actually Cover

Those exam risks point to the same root cause: program architecture that wasn't built before the technology was deployed. The right consulting priority at the startup stage is building that foundation first — treating policy, process, and technology as a single integrated system rather than three separate workstreams.

The most valuable AI applications at this stage:

- Transaction monitoring rule calibration: setting thresholds appropriate for the startup's specific transaction types and customer risk profile, not copying enterprise templates built for different business models

- Customer risk scoring: designing a risk rating methodology that can be documented, defended, and updated as the customer base evolves

- KYC/KYB onboarding workflows: building automated processes with sufficient documentation to demonstrate program intent to examiners

The engagement model that works is a senior-led advisory approach covering policy development, risk assessment design, and monitoring setup in one integrated engagement. Pillars FinCrime Advisory is built for exactly this stage, offering CAMS-certified expertise across the full compliance lifecycle without the enterprise-sized scope that most startups don't need.

What Exam Readiness Looks Like at the Startup Stage

A startup facing its first regulatory examination needs more than a transaction monitoring tool. Examiners evaluate whether the program is operational and defensible — not just whether technology is present.

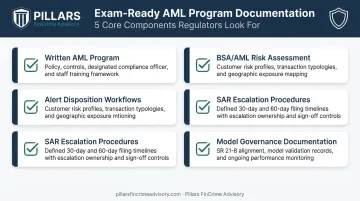

Exam-ready documentation at the startup stage typically includes:

- A written AML program with internal policies, controls, a designated compliance officer, training records, and an independent review plan (per 31 CFR 1022.210)

- A documented BSA/AML risk assessment covering customer types, transaction types, and geographic exposure

- Alert disposition workflows with documented decision logic

- SAR escalation procedures with timeline controls (30-day filing requirement for identified suspects; 60 days when no suspect is identified)

- Model governance documentation for any AI-assisted monitoring, consistent with SR 21-8 guidance on model risk management

The principle that matters most at this stage: people and process must be built alongside the technology. An AI tool without documented governance is a liability in an exam, not an asset.

AI Consulting for Mid-Market Companies: Scaling What Works

The Mid-Market Problem

Established fintechs and payments companies often reach a point where the compliance program they built in year one can't sustain the transaction volume, product complexity, or partner relationships of year three or four. The program works — just not at scale.

The symptoms are recognizable:

- High false positive rates consuming analyst capacity

- Alert backlogs that delay SAR filing timelines

- Inconsistent alert disposition across reviewers

- Risk segmentation logic that hasn't been updated since launch

- Board reporting that doesn't demonstrate program effectiveness

98% of financial institutions reported increased financial crime compliance costs in LexisNexis Risk Solutions' 2023 financial crime compliance study — a figure that reflects exactly the kind of pressure mid-market AI consulting is designed to relieve.

What Mid-Market AI Consulting Should Actually Cover

At this stage, the consulting challenge is diagnosing which parts of an existing program are creating friction — then using AI to reduce it without introducing new regulatory risk.

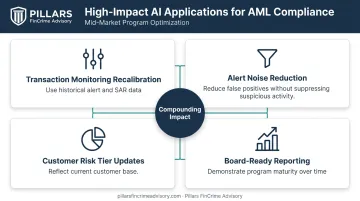

The most impactful AI applications for mid-market compliance programs:

- Recalibrate transaction monitoring scenarios and thresholds using historical alert and SAR data — not generic industry benchmarks

- Reduce alert noise without suppressing legitimate suspicious activity, which requires deep program knowledge, not just technical implementation

- Update customer risk tiers to reflect the current customer base, not the one the company had at launch

- Build board-ready reporting metrics that demonstrate program maturity and improvement over time

These improvements compound. Better alert quality reduces analyst backlog; refined segmentation reduces false positives upstream. Addressing them together is where AI consulting at the mid-market level delivers the most durable results.

The Knowledge Transfer Imperative

The mid-market-specific risk that often goes unaddressed is consultant dependency. The right engagement leaves the internal team more capable — with documented processes and governance frameworks they own outright.

The 2024 Federal Reserve enforcement action against Evolve Bank required an independent transaction monitoring validation and a transaction review of fintech-partner wire activity — obligations the institution had to execute and sustain internally.

External consultants can design and build improvements, but the internal team has to defend them in an examination.

A mid-market engagement should produce:

- Documented model validation results with updated governance controls

- Revised alert disposition procedures the team can follow consistently

- Updated risk assessment tied to current product and customer profile

- Board reporting templates that demonstrate ongoing program oversight

Choosing the Right AI Consulting Strategy

The Four Decision Factors

Before selecting a consulting model, answer these four questions honestly:

- Program maturity — Does a foundational compliance program exist, or does one need to be built?

- Regulatory timeline — Is an exam imminent, or is there runway to build systematically?

- Internal bandwidth — Does the team have capacity to absorb and operate what the consultant builds?

- Growth trajectory — Will the solution need to scale 2–5x in the next 24 months?

Situational Guidance

Choose a startup-oriented consulting model when:

- The AML program exists on paper but hasn't been operationalized

- Transaction monitoring hasn't been configured to the company's business model

- The organization needs audit-ready documentation before its first examination

- Growth is creating pressure to add AI tools before the foundation is solid

Choose a mid-market consulting model when:

- The program exists but alert volumes are unsustainable

- SAR quality or filing timelines are inconsistent

- A regulatory examination is approaching and current metrics don't demonstrate program maturity

- Product expansion has outpaced risk segmentation logic

The Hybrid Scenario

Some fintechs don't fit cleanly into either category. A company that scaled rapidly may have a program designed for its first year of operations trying to support its third or fourth year of volume. These organizations need elements of both approaches. The right starting point is a candid program assessment — not a technology shortlist.

Pillars FinCrime Advisory works directly with compliance leadership and boards across both phases — build and optimization — translating regulatory expectations into practical program decisions.

Whether an organization is in its first year of operation or preparing for an examination after significant growth, the engagement begins the same way: an honest assessment of where the program actually stands today.

Real-World Scenarios: Putting the Strategy Into Practice

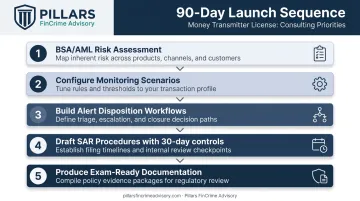

Scenario 1 — Startup: Launching with a New Money Transmitter License

A payments company receives its money transmitter license and needs to go live within 90 days. It has a BSA officer on paper and a vendor contract for transaction monitoring software, but no configured rules, no documented risk assessment, and no alert disposition workflow.

The consulting priorities, in order:

- Complete the BSA/AML risk assessment covering customer types, transaction types, and geographic profile

- Configure monitoring scenarios calibrated to the company's specific transaction types — not enterprise defaults built for different business models

- Build alert disposition workflows with documented decision logic and escalation triggers

- Draft SAR procedures with 30-day filing controls

- Produce exam-ready documentation demonstrating that program decisions were made deliberately, not by default

The AI tools available don't determine success here. The documentation demonstrating how those tools were configured and governed does.

Scenario 2 — Mid-Market: Facing an Exam with an Alert Backlog

An established fintech with three years of transaction monitoring history is approaching a regulatory examination. Alert volume has doubled in 18 months, the team is behind on disposition, and SAR narratives are inconsistent. The compliance team knows the program works — but can't demonstrate it in a format examiners will find compelling.

The consulting priorities:

- Pull historical alert and SAR data to identify which monitoring scenarios are generating noise versus legitimate activity

- Retune thresholds using actual performance data, with documented rationale for every change

- Update risk segmentation to reflect the current customer base

- Build board-facing metrics that show improvement trajectory, not just current state

- Document the tuning methodology so internal staff can defend it during examination

Both scenarios share a common measure of success: the consulting engagement produces a program the internal team can operate independently, defend under regulatory scrutiny, and scale as the business grows. That outcome requires more than tool selection — it requires documented governance, defensible methodology, and deliberate program design from day one.

Conclusion

The choice between startup-oriented and mid-market AI consulting comes down to one practical question: does a compliant, operational compliance program exist, or does one need to be built?

The right consulting model depends on where your program stands today:

- Startups need a partner who constructs a defensible foundation from the ground up — policy, risk assessment, monitoring configuration, and governance documentation built as a system, not assembled after the fact.

- Mid-market companies need a partner who diagnoses what's creating friction, tunes what already exists, and demonstrates measurable improvement without disrupting regulatory continuity.

Choosing the wrong model carries real consequences: program deficiencies that surface during examinations, remediation obligations with compressed timelines, and enforcement exposure that far exceeds the original consulting investment. The 2024 FDIC Thread Bank order required a qualified AML officer within 60 days, a risk assessment within 90 days, and a full AML plan within 120 days — timelines that become achievable only when the foundational work is already in place. Getting the consulting model right from the start is what makes the difference between managing a regulatory event and being overwhelmed by one.

Frequently Asked Questions

What is the 10-20-70 rule for AI?

The 10-20-70 rule holds that 10% of AI success comes from algorithms, 20% from technology and data, and 70% from people and processes — a framework documented in BCG's 2024 AI transformation guidance. In compliance, this means the human layer — documented workflows, governance ownership, and trained staff — determines whether AI-assisted monitoring is defensible to regulators, not the sophistication of the tool itself.

Which AI is best for fintech startups?

For fintech startups, the right AI tool is the one calibrated to the organization's specific transaction types, customer risk profile, and team capacity. A compliance consultant helps right-size the selection before deployment, ensuring the program foundation is strong enough to use the tool effectively rather than generating unmanageable alert volumes from day one.

What is the difference between AI consulting for startups and mid-market companies in financial services?

Startup consulting focuses on building a foundational, scalable compliance program from scratch — covering policy, risk assessment, monitoring configuration, and exam-ready documentation. Mid-market consulting focuses on optimizing and scaling an existing program, with different engagement models, timelines, and priorities at each stage.

When should a fintech startup hire an AI compliance consultant?

The best time is before or during the program build phase — before transaction volume outpaces manual controls. Programs designed to scale from the start are far less expensive than programs retrofitted under regulatory pressure, and regulators can distinguish between the two.

How do mid-market financial institutions use AI in their compliance programs?

The most common applications are transaction monitoring model tuning, alert quality improvement, risk-based customer segmentation, and automated board reporting workflows. Each requires deep program knowledge to implement without introducing new regulatory risk.

How much should a fintech startup budget for AI compliance consulting?

Early-stage fintech compliance program builds typically range from $15,000 to $60,000, depending on business model complexity and the number of workstreams required. That's far less than the remediation costs triggered by a program deficiency finding — making early investment the more cost-effective path.