Introduction

Fintech innovation moves fast. Regulators are moving faster — and the cost of falling behind is no longer just a fine. Program shutdowns, lost bank partnerships, and lasting reputational damage are now live outcomes for compliance failures.

The numbers make the stakes clear. According to Alloy's 2023 State of Compliance Benchmark Report, 93% of fintechs find meeting compliance requirements challenging — and over 60% paid at least $250,000 in compliance fines in the prior year. These aren't outliers. They reflect what happens when compliance programs fall behind business growth.

This guide covers what fintech compliance actually requires: the four major risk categories every leadership team must understand, the key US regulations that apply regardless of business model, and how to build a program that's both audit-ready and scalable. Whether you're early-stage or heading into your first regulatory exam, you'll come away with a clear map of what examiners expect — and where programs typically break down.

Key Takeaways

- Fintech compliance spans multiple obligations — AML, KYC/KYB, OFAC, consumer protection, and data security — and your specific mix depends on products, customers, and markets.

- Four risk categories demand proactive attention: regulatory, cybersecurity/third-party, financial/operational, and reputational.

- Non-compliance costs extend beyond fines — they can end bank partnerships and trigger examinations.

- Scalable compliance programs are built on documented policies, risk assessments, transaction monitoring, and independent testing.

- Compliance maturity is a competitive signal — to examiners, bank partners, and investors.

What Fintech Compliance Really Means for Your Business

Fintech compliance isn't a single regulation. It's a layered set of legal, financial crime, data protection, and consumer protection obligations that shift based on what products you offer, who your customers are, and where you operate.

A payments company has a different compliance footprint than a lending platform or a crypto exchange. Multi-state operations add state-level licensing, lending laws, and data privacy rules on top of federal obligations. The compliance map changes every time the business model does — and that scope expands further when bank partnerships are involved.

The Bank-Grade Standard Misconception

One of the most common misunderstandings among fintech leadership: the assumption that compliance obligations are lighter when you're not a licensed financial institution.

That's not how regulators or bank sponsors see it. Fintechs that operate as vendors or program partners to regulated institutions are held to bank-grade compliance standards as a baseline condition of those relationships. Regulators have made this explicit — enforcement actions against Blue Ridge Bank, Cross River Bank, and Evolve Bank & Trust all centered on deficient oversight of fintech partners, signaling that the compliance bar for the fintech extends directly from the bank's obligations.

Compliance as a Business Investment

A mature compliance program does more than prevent fines. It:

- Reduces examination risk and shortens remediation timelines

- Supports bank partnership eligibility and ongoing sponsor relationships

- Demonstrates organizational credibility to investors and counterparties

- Creates a governance structure that scales alongside the business

Where compliance sits in the organization determines how well it keeps pace with the business. Programs treated as a back-office cost center tend to fall behind product velocity. Programs built as a strategic function stay aligned with growth — and are far better positioned when regulators come knocking.

The Four Major Compliance Risks Fintechs Face

These four risk categories don't operate in isolation. A single cybersecurity incident can trigger regulatory action, erode consumer trust, and put bank partnerships at risk — sometimes simultaneously. Understanding how they connect matters as much as understanding each one on its own.

Regulatory Risk

The US regulatory landscape for fintechs is fragmented by design — no single unified framework governs the industry. Depending on your business model, you may answer to the CFPB, FinCEN, OCC, FDIC, SEC, FTC, and state-level regulators simultaneously, each with different examination priorities and enforcement approaches.

Enforcement actions have accelerated. The CFPB ordered Block/Cash App to pay $120 million in consumer refunds and a $55 million penalty for fraud-response failures. Chime was ordered to pay a $3.25 million civil money penalty and at least $1.3 million in redress for delaying customer refunds. The Federal Reserve fined Green Dot $44 million for consumer compliance breakdowns.

Operating across multiple states compounds this exposure. Each state may impose its own licensing requirements, lending laws, or data privacy rules — and inadequate compliance infrastructure in any one jurisdiction creates risk across the entire operation.

Cybersecurity and Third-Party Risk

Fintechs hold dense concentrations of financial and personal data, which makes them attractive to both external attackers and malicious insiders. The Block/Cash App incident illustrates the insider threat: a former employee downloaded reports containing information on approximately 8.2 million current and former Cash App Investing customers, which Block disclosed in an SEC Form 8-K filing.

External dependencies introduce a separate attack surface. Fintechs rely on:

- APIs connecting to banking partners and data providers

- Cloud infrastructure housing transaction records and customer data

- Vendor networks spanning KYC tools, payment processors, and fraud platforms

A weakness anywhere in that chain becomes your compliance problem. OCC, the Federal Reserve, and FDIC addressed this directly in their June 2023 interagency guidance on third-party risk management — establishing that vendor due diligence and ongoing oversight are compliance obligations, not optional best practices.

Financial, Operational, and Reputational Risk

Moving fast without adequate controls creates predictable exposure:

- Fraud and transaction errors — weak controls in high-volume environments create financial crime gaps that attract examiner attention

- Capital and operational shortfalls — growth without infrastructure strains the controls meant to catch problems before they escalate

- Reputational damage — compliance failures at one fintech affect trust in the broader ecosystem; for companies dependent on consumer confidence and bank partnerships, a single high-profile incident can unwind years of brand-building

Key Regulations Every US Fintech Must Understand

The specific regulatory obligations depend on your business model, customer base, and markets. That said, several frameworks apply broadly, and identifying which ones apply to your operation is the first task any compliance-minded leadership team must complete.

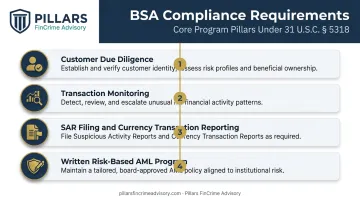

AML, BSA, and KYC/KYB Obligations

The Bank Secrecy Act (BSA) is the foundation of US anti-money laundering compliance. It requires covered financial institutions and their fintech partners to implement:

- Customer due diligence (CDD) at onboarding and ongoing

- Transaction monitoring for suspicious activity

- Suspicious Activity Report (SAR) filing and currency transaction reporting

- A written, risk-based AML program

FinCEN enforces these requirements aggressively. In 2025, FinCEN assessed a $37 million civil money penalty against Brink's Global Services USA for BSA violations including failure to register as a money services business, maintain an effective AML program, and file SARs. NYDFS separately secured a $40 million settlement with Block for BSA/AML compliance failures on the Cash App platform.

KYC (Know Your Customer) and KYB (Know Your Business) are the identity verification backbone of BSA compliance, covering onboarding checks, beneficial ownership verification, and ongoing monitoring. KYC confirms who an individual customer is; KYB extends that to business entities and their controlling ownership.

Deficiencies in both are among the most frequently cited findings in fintech enforcement actions.

OFAC Sanctions and Consumer Protection Laws

OFAC sanctions screening is mandatory for any fintech that processes payments or onboards customers. Real-time screening against prohibited lists, a documented compliance program, and clear escalation procedures represent baseline requirements. The enforcement record shows fintechs aren't exempt: Payoneer settled with OFAC for $1.4 million in 2021, and daVinci Payments settled for $206,213 in 2023, both involving payments processed for parties in sanctioned jurisdictions.

Sanctions exposure sits at the payment layer. Consumer protection obligations, by contrast, run through the product layer — and they apply broadly to any fintech offering consumer-facing financial products:

- UDAP/UDAAP — prohibits unfair, deceptive, or abusive acts in marketing, disclosures, and product terms

- CFPB authority — extends to nonbank financial companies that pose risks to consumers

- ECOA and TILA — apply to lending-related fintechs covering credit discrimination and lending disclosures

Data Security and Reporting Frameworks

| Framework | Key Obligation | Applies To |

|---|---|---|

| GLBA Safeguards Rule | Written information security program; breach notification for 500+ affected persons | Financial institutions handling nonpublic personal information |

| PCI DSS v4.0.1 | Documented controls for cardholder/account data security | Any fintech handling card data |

| CCPA/CPRA | Data rights, deletion, opt-out of sale | Fintechs serving California residents |

| GDPR | Data rights, breach notification, processing requirements | Fintechs serving EU residents |

The FTC strengthened the GLBA Safeguards Rule in 2021, with amended requirements effective June 2023, adding mandatory breach reporting for security events affecting 500 or more people. Fintechs that haven't benchmarked their data security programs against the updated rule face real exposure in the next regulatory exam cycle.

How to Build a Scalable Fintech Compliance Program

Building a compliance program isn't just hiring a compliance officer. It requires a documented governance structure, risk-based policies, operational controls, and a testing framework designed to grow alongside the business. A program that works at 10,000 monthly transactions won't automatically work at 10 million.

Foundational Program Elements

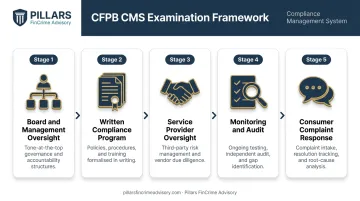

Regulators and bank sponsors evaluate compliance management systems (CMS) against a consistent set of expectations. The CFPB's CMS examination framework specifically assesses:

- Board and management oversight — evidence that leadership sets compliance expectations and receives regular reporting

- Written compliance program — documented policies, procedures, and a risk assessment methodology

- Service provider oversight — documented vendor due diligence and ongoing monitoring

- Monitoring and audit — independent testing of controls, not just written policies

- Consumer complaint response — a process for capturing, escalating, and resolving complaints

The distinction between written policies and functioning controls matters enormously during examinations. Examiners look for documented testing results, issue tracking logs, training records, and governance reporting — evidence that the program operates as described.

Building for Audit Readiness and Scale

Audit readiness is an ongoing posture, not a pre-exam sprint. Key components include:

- Periodic independent testing of compliance controls across the program

- Alert quality reviews for transaction monitoring, calibrated to the company's specific risk profile

- Regular risk assessment updates as products, markets, and customer types evolve

- Governance reporting to the board or senior leadership on compliance performance and issues

Transaction monitoring calibration deserves specific attention. Alert volumes set too high create operational burden and analyst fatigue; set too low, they miss real risk. Either way, miscalibration signals program immaturity to examiners.

The FFIEC BSA/AML Examination Manual is explicit on this point: automated monitoring systems must be validated to ensure models detect potentially suspicious activity. SAR content quality is a direct indicator of overall program health.

Fintechs building or maturing their compliance programs often need outside expertise to translate regulatory expectations into operational reality. Pillars FinCrime Advisory works directly with fintech and payments leadership on policy development, risk assessments, transaction monitoring optimization, and exam preparation — practical support designed to scale with the business, not just check boxes.

Best Practices for Sustaining Compliance as You Grow

Set the Tone from the Top

Boards and C-suite executives determine whether compliance is a strategic priority or a back-office checkbox. Regulators assess governance maturity directly — weak tone at the top is itself a finding, not just a contributing factor. Establishing board-level compliance reporting, clear escalation paths, and documented accountability for compliance outcomes signals program maturity to examiners and stakeholders alike.

Build Continuous Monitoring into Operations

Compliance is not annual. A sustainable compliance posture requires:

- Real-time transaction monitoring tuned to the company's risk profile

- Periodic risk reassessments whenever products or markets change

- Ongoing staff training with documented completion records

- A defined process for escalating and resolving compliance issues before they become regulatory problems

Engage Regulators Proactively

Fintechs that treat regulators as adversaries tend to fare worse during examinations than those who demonstrate genuine responsiveness. Several formal channels exist specifically for fintech engagement:

- FinCEN operates an Innovation Hours Program for fintech and RegTech companies

- CFPB maintains No-Action Letter and Compliance Assistance Sandbox policies

- OCC established an Office of Financial Technology in 2023 to engage with bank-fintech arrangements and emerging technologies

Participating in guidance processes, responding to examination findings transparently, and demonstrating continuous improvement builds regulatory confidence — and that confidence translates directly into lower examination risk as your business scales.

Frequently Asked Questions

What regulations apply to fintech?

US fintechs are subject to a range of obligations depending on their services and customers. Core frameworks include BSA/AML, KYC/KYB, and OFAC sanctions screening. Consumer protection laws (UDAP/UDAAP, ECOA, TILA) apply to consumer-facing products, while GLBA, PCI DSS, CCPA, and GDPR add data security and privacy obligations based on the data handled and markets served.

What are the biggest compliance risks for fintech companies?

The four major risk categories are regulatory exposure from a fragmented multi-agency landscape, cybersecurity and third-party vendor risk, operational risk from rapid growth without adequate controls, and reputational damage from compliance failures. These categories are interconnected: a failure in one typically creates exposure in others.

What is the difference between AML and KYC compliance in fintech?

KYC (Know Your Customer) is the identity verification component of onboarding — confirming who a customer is and assessing their risk profile. AML (Anti-Money Laundering) is the broader ongoing program: transaction monitoring, suspicious activity detection, SAR filing, and reporting designed to prevent financial crime from occurring through your platform.

How do fintechs prepare for regulatory exams?

Exam readiness requires documented policies, current risk assessments, testing records, training logs, and governance reporting. Examiners evaluate whether controls are actually functioning, not just whether they exist on paper. Fintechs that demonstrate continuous improvement and active issue tracking consistently fare better than those presenting static documentation.

When does a fintech need a dedicated compliance officer?

Any fintech processing meaningful transaction volumes, maintaining bank partnerships, or operating in regulated lending or payments markets needs designated compliance ownership. Early-stage companies often rely on fractional or advisory support — but compliance accountability should never be an afterthought, regardless of stage. Pillars FinCrime Advisory's fractional CCO/BSA Officer service is built specifically for this need.

How does fintech compliance differ from traditional bank compliance?

The underlying regulatory obligations are often identical. The difference is context: fintechs typically face faster growth, leaner teams, and greater reliance on technology. That requires compliance programs built to scale from the start — with automated monitoring, documented governance structures, and the flexibility to adapt as products and markets evolve.