Introduction

A financial crime risk assessment is a structured, documented process through which financial institutions and fintechs identify, evaluate, and prioritize their exposure to financial crimes — money laundering, fraud, terrorist financing, and sanctions violations.

For compliance officers, BSA/AML teams, fintech leadership, and boards, this isn't a peripheral compliance task. The risk assessment is the foundation of any credible financial crime compliance program. Every downstream control decision — transaction monitoring thresholds, CDD procedures, sanctions screening parameters — should trace back to it.

Given that centrality, the risk assessment is also consistently mishandled. Many organizations treat it as a box to check rather than a living diagnostic framework. Others adopt generic templates that describe hypothetical risks instead of actual exposure.

The result: miscalibrated controls, resource misallocation, and examination findings that cite the risk assessment as the root cause of broader program deficiencies.

What separates an audit-ready assessment from a checkbox exercise comes down to methodology, scope, and how the findings actually drive program decisions. This guide breaks down each of those dimensions.

Key Takeaways

- A financial crime risk assessment is a living framework, not an annual filing — it drives controls, policies, and examiner conversations.

- Effective assessments follow a defined sequence: identify inherent risk, evaluate controls, calculate residual risk, and document findings.

- FFIEC, FATF, and FinCEN all expect institutions to maintain a written, risk-based assessment tailored to their business model.

- Generic, copy-paste assessments fail examiner scrutiny — the risk profile must reflect the firm's actual exposure.

- Fintech-specific risks require explicit documentation and compensating controls — not boilerplate coverage.

What Is a Financial Crime Risk Assessment?

A financial crime risk assessment is a documented analysis of a firm's unique exposure to ML/TF, fraud, bribery, sanctions violations, and related financial crimes. What distinguishes it from a general compliance audit is its explicit focus on measuring risk before controls are applied (inherent risk) and after (residual risk).

Inherent Risk vs. Residual Risk

These two concepts anchor every credible risk assessment:

- Inherent risk — the raw exposure a firm faces based on its business model, customer base, products, and geography, before any compliance controls are considered

- Residual risk — what remains after the effectiveness of existing controls is factored in

The gap between inherent and residual risk is where your compliance program lives. Strong controls can bring high inherent risk down to an acceptable level — but weak controls against even moderate exposure will draw examiner scrutiny. That gap is what regulators are actually evaluating.

Risk Assessment vs. AML Compliance Program

These are related but serve different functions:

| Component | Role |

|---|---|

| Risk Assessment | Diagnoses the risk landscape — identifies what risks exist and how severe they are |

| AML Compliance Program | Addresses the risks — policies, transaction monitoring, CDD, training, and other controls |

As the FFIEC BSA/AML Examination Manual states, a well-developed risk assessment helps institutions identify ML/TF and other illicit finance risks and develop appropriate internal controls. Neither can be properly designed without the other — the assessment shapes the program, and the program's effectiveness feeds back into the next assessment cycle.

Why Financial Institutions and Fintechs Must Have One

The Regulatory Imperative

Three regulatory frameworks establish the baseline requirement for a formal risk assessment:

- Bank Secrecy Act (31 USC 5318(h)(1)): Requires financial institutions to establish anti-money laundering programs.

- 31 CFR Chapter X: Mandates written, risk-based AML programs for banks, MSBs, and broker-dealers.

- FATF Recommendation 1: Requires countries and institutions to identify, assess, and understand money laundering and terrorist financing (ML/TF) risks and apply a risk-based approach.

The FFIEC treats the BSA/AML risk assessment as a supervisory expectation — and critically, if an institution's risk assessment is absent or inadequate, examiners will develop one themselves. That's not a position any institution wants to be in.

What Enforcement Actions Reveal

Recent enforcement actions show exactly what's at stake when risk assessments fail:

- TD Bank (2024): FinCEN's consent order cited insufficient processes for identifying and assessing high-risk customers, including unmonitored peer-to-peer payment activity. Civil money penalty: $1.3 billion. Source: FinCEN TD Bank Consent Order

- Blue Ridge Bank (2024): The OCC cited failure to assess inherent risks from fintech partners and subpartners, restricted new fintech relationships, and required a comprehensive BSA risk assessment program.

- Customers Bancorp (2024): The Federal Reserve cited significant BSA/AML deficiencies tied to the bank's digital asset and tokenized payment activities — risks that weren't adequately reflected in the institution's risk framework.

These aren't isolated incidents. Each action points to the same root problem: a risk framework that didn't keep pace with the institution's actual risk profile.

The Fintech Gap

For fintechs and payments companies, the stakes are even higher. Novel business models, app-based delivery, rapid customer growth, and third-party partnerships create risk profiles that differ substantially from traditional banks. Examiners understand this distinction well. The OCC's Blue Ridge action made it explicit: failure to assess inherent risks from fintech partner relationships is a cited deficiency, not a technicality.

How to Conduct a Financial Crime Risk Assessment

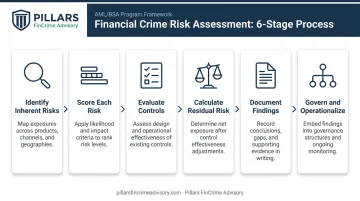

The process follows a clear conceptual flow:

Identify inherent risks → Score each risk → Evaluate controls → Calculate residual risk → Document findings → Govern and operationalize

The FFIEC does not require a specific format or methodology. Smaller fintechs may use an impact-only rating model, while larger institutions typically apply a likelihood-times-impact risk matrix. What regulators consistently expect is documented rationale — not a particular template.

Inputs must draw from both internal data (transaction activity, SAR trends, CDD exceptions) and external sources (FATF typologies, FinCEN advisories, OFAC lists, national risk assessments).

Step 1 — Identify Inherent Risk Across All Risk Categories

Document each major risk category — customers, products/services, delivery channels, and geographies — and identify the specific ML/TF vulnerabilities associated with each.

This requires actual business data. What types of customers does the firm serve? What products does it offer? How are services delivered? Where do transactions flow? The FFIEC specifies that risk categories should be unique to the institution — a point that directly undermines generic template approaches.

Step 2 — Assess and Score Each Risk

For each identified risk, assess:

- Impact — the severity of harm if the risk is exploited

- Likelihood — the probability of occurrence (for more complex businesses)

The combination produces an inherent risk rating, typically Low / Medium / High or a numeric scale (1–5). The methodology should be applied consistently across all risk areas and documented clearly enough that a third party (including an examiner) can follow the logic.

Step 3 — Evaluate Controls and Calculate Residual Risk

With inherent risk scores in hand, the next step is assessing whether current controls are adequate to reduce that exposure. Evaluate whether each control is:

- Adequately designed — does the control address the identified risk?

- Operating effectively — is the control functioning as intended in practice?

Controls to evaluate include transaction monitoring rules, CDD/EDD procedures, sanctions screening, training programs, and suspicious activity reporting processes. Where control effectiveness falls short of inherent risk scores, residual risk is elevated — and those gaps become your remediation priorities.

Step 4 — Document, Approve, and Operationalize

The FFIEC manual is clear: documenting the risk assessment in writing is sound practice, and it should be distributed to business lines, the board, management, and relevant staff.

Practically, this means:

- Formal written documentation with clear risk ratings, control assessments, and gap findings

- Review and approval by senior management and the board

- Distribute it to all relevant business units

- A defined process for interim updates when material changes occur

Treat the risk assessment as a living document. New product launches, market expansions, high-risk customer onboarding, and material regulatory guidance all trigger an update — waiting for the annual cycle means operating with an outdated picture of your actual exposure.

Key Risk Categories Every Assessment Must Cover

The FFIEC, FATF, and the Wolfsberg Group consistently identify four core risk dimensions. Gaps in any one of them are a cited program deficiency — not a theoretical oversight.

Customer Risk

Firms must assess the ML/TF risk posed by each customer type they serve. The FFIEC notes that not all PEPs are automatically higher risk — the rating depends on facts and circumstances — but certain customer types warrant documented elevated risk consideration:

- Politically exposed persons (PEPs) and their associates

- Non-resident and foreign account holders

- Customers with complex or opaque ownership structures

- Industries that historically present elevated ML/TF exposure

Each customer segment in the assessment should include a documented rationale for its risk rating, with supporting facts tied to specific customer characteristics — not a generic tier assignment.

Product and Service Risk

Each product or service carries its own inherent risk profile based on factors like transaction velocity, anonymity potential, cross-border capability, and cash intensity. Products that consistently appear in FFIEC risk assessment examples and enforcement actions include:

- International wire transfers

- Peer-to-peer payment functionality (explicitly cited in the TD Bank FinCEN order)

- Digital assets and tokenized payment products (cited in the Customers Bank Federal Reserve action)

- Electronic banking and remote deposit capture

Delivery Channel Risk

How services are delivered affects risk. The FFIEC manual states directly that accounts opened without face-to-face contact may carry higher ML/TF risk.

FATF's 2020 digital identity guidance clarifies that non-face-to-face onboarding is not automatically high-risk when reliable, independent digital ID systems are used. For fintechs relying on app-based onboarding, the key is documentation: record both the elevated channel risk and the compensating controls that offset it — document verification, liveness detection, and identity proofing.

Third-party-introduced relationships add another layer of risk that assessments must address explicitly. As the Blue Ridge Bank OCC order demonstrated, failure to assess risks from fintech subpartner arrangements is a cited deficiency — not a theoretical gap.

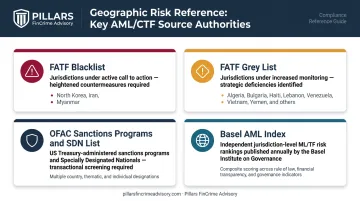

Geographic Risk

Firms must assess where they operate, where customers are located, and where transactions flow. Authoritative reference sources for geographic risk include:

- FATF blacklist — as of February 2026: North Korea, Iran, and Myanmar

- FATF grey list — as of February 2026: includes Algeria, Bulgaria, Haiti, Lebanon, Venezuela, Vietnam, Yemen, and others

- OFAC sanctions programs and SDN list

- Basel AML Index — provides jurisdiction-level ML/TF risk rankings

High-risk geographic exposures require documented EDD protocols with clear ownership — which examiner reviews the exposure, what additional information is collected, and how that information is retained.

Financial Crime Risk Assessment Best Practices

Build Around Your Actual Business Model

A payments company processing peer-to-peer transfers faces fundamentally different risks than a community bank offering personal checking. The assessment must reflect that specificity — not a generic industry template — to withstand examiner scrutiny.

That specificity is where firms like Pillars FinCrime Advisory add practical value: structuring the initial risk assessment around the firm's real product set, customer segments, and delivery channels rather than adapting a boilerplate document that describes someone else's risk profile.

Link Every High-Risk Finding to a Specific Control

Every elevated-risk area needs a corresponding documented control. If the assessment rates PEP exposure as high-risk but the EDD program doesn't address PEPs specifically, that gap will be visible to examiners.

The FFIEC expects a clear, traceable connection between what the risk assessment identifies and how the compliance program responds. A risk assessment that sits in a SharePoint folder without informing transaction monitoring rules, CDD thresholds, or training content has no operational value.

Establish Governance Accountability

The FFIEC recommends that the risk assessment be provided to the board of directors, management, and appropriate staff. Board-level review and documented approval demonstrates program maturity and confirms that senior leadership is engaged with the firm's financial crime risk profile.

Fintechs without a formal compliance committee can fill that gap with fractional CCO or BSA Officer services. This provides the governance structure needed to conduct and approve the assessment appropriately, so the process isn't delegated entirely to a junior analyst without executive accountability.

Set a Review Cadence with Defined Triggers

There is no regulatory mandate for a specific update frequency — the FFIEC states there is no requirement for continuous or specified periodic updates. Best practice, however, is:

- Annual review at minimum

- Triggered interim updates when the firm launches new products, enters new markets, acquires new business lines, onboards a new high-risk customer segment, or receives material regulatory guidance

Common Mistakes That Undermine Financial Crime Risk Assessments

The Copy-Paste Problem

Many fintechs conducting their first formal risk assessment adopt a generic template without tailoring it to their actual risk profile. The result is a document describing hypothetical risks — not the firm's real exposure. Experienced examiners recognize this immediately. The FDIC's Shinhan Bank order made explicit that a compliant risk assessment must include detailed qualitative and quantitative analysis of the bank's actual risk profile, with documented reassessment policies.

Disconnect Between Assessment and Program

A risk assessment that doesn't actively inform your compliance program has no operational value. Regulators expect a clear, traceable link between identified risks and program design — specifically:

A risk assessment that doesn't actively inform your compliance program has no operational value. Regulators expect a clear, traceable link between identified risks and program design — specifically:

- Transaction monitoring rules and alert thresholds

- Customer due diligence (CDD) and enhanced due diligence (EDD) standards

- Staff training content and frequency

- Policies governing higher-risk products or customer segments

Document those connections explicitly. Examiners will ask for them, and "it's implied" is not a defensible answer.

The "New Date" Update

Simply changing the date on last year's document doesn't constitute an updated risk assessment if the firm's products, customers, or operating environment have materially changed. Residual risk scores that never shift year over year — regardless of business growth, new product launches, or regulatory alerts — are a red flag examiners frequently cite in examination findings. If your scores look identical to last year's, expect that question in your next exam.

Avoiding these mistakes is straightforward once you know what a defensible, examiner-ready assessment actually looks like.

Frequently Asked Questions

What is a financial crime risk assessment?

A financial crime risk assessment is a structured process through which a financial institution or fintech identifies, analyzes, and scores its exposure to money laundering, fraud, terrorist financing, and sanctions violations. It serves as the foundation for a risk-based compliance program and is the primary lens regulators use to evaluate whether that program is appropriately calibrated.

How often should a financial crime risk assessment be updated?

There is no regulatory mandate for a fixed update frequency. Best practice is an annual review at minimum, with interim updates triggered by material business changes — new product launches, geographic expansion, acquisitions, new high-risk customer segments, or material regulatory guidance relevant to the firm's risk profile.

What is the difference between inherent risk and residual risk?

Inherent risk is the level of risk a firm faces before any compliance controls are applied. Residual risk is what remains after controls such as transaction monitoring, CDD, and sanctions screening are factored in. A well-designed compliance program aims to reduce residual risk to an acceptable level relative to the firm's risk appetite.

Who is responsible for conducting a financial crime risk assessment?

The BSA Officer or Chief Compliance Officer typically leads the process, but the assessment requires input from product, operations, and technology teams. It should be reviewed and approved by senior leadership or the board to demonstrate governance accountability — not delegated entirely to the compliance function.

What happens if a bank or fintech has an inadequate risk assessment?

An inadequate risk assessment can trigger examination findings, Matters Requiring Attention (MRAs), or enforcement actions. Regulators use the risk assessment to evaluate the entire compliance program, so deficiencies cascade — weaknesses in transaction monitoring, CDD, and other controls frequently trace back to a deficient risk assessment.

How is a financial crime risk assessment different from an AML compliance program?

The risk assessment is the diagnostic tool: it identifies what risks exist and how severe they are. The AML compliance program is the operational framework — policies, procedures, controls, and training — designed to address those risks. Without the risk assessment, the compliance program cannot be properly calibrated.