The challenge is that AI cuts both ways. It gives compliance and risk teams genuinely powerful tools to catch fraud faster, score members more accurately, and reduce the manual burden on stretched compliance staff. But it also introduces risks that didn't exist before: model bias that can produce discriminatory outcomes, data privacy exposure, vendor dependency that creates concentration risk, and regulatory scrutiny from examiners who are paying close attention.

For credit union compliance and risk leaders, the question is no longer whether to engage with AI — it's how to do so without creating the very problems you're trying to prevent.

Key Takeaways

- AI is actively deployed across AML transaction monitoring, credit risk scoring, fraud detection, and member identity verification in credit unions.

- Credit unions face four AI risk categories: financial, reputational, operational, and legal/regulatory.

- The NCUA has not issued AI-specific regulations, but existing technology-neutral rules fully apply — and examiners are paying attention.

- AI governance demands board-level oversight, a documented use case inventory, model validation, and thorough vendor due diligence.

- SAR filing practices and CIP procedures must be updated to account for AI-enabled fraud typologies, including deepfakes.

How AI Is Changing Risk Assessment in Credit Unions

From Static Rules to Adaptive Models

Traditional AML transaction monitoring worked on fixed thresholds — a transaction over a certain amount, a structuring pattern, a known typology. The problem with rules-based systems is that they don't adapt. Bad actors do.

Machine learning models change that dynamic. Instead of checking transactions against static rules, they learn behavioral baselines for each member and flag deviations in near real time. The impact on false positive rates is significant: according to McKinsey, traditional AML transaction monitoring models often carry false-positive rates above 98%, while advanced risk-rating models can reduce incorrectly labeled high-risk customers by 25% to 50%. For compliance teams drowning in alerts, that translates to a dramatic reduction in manual workload.

FATF has also recognized that AI and ML can help identify complex AML/CFT cases that static rules miss, though it notes that explainability gaps can undermine confidence in justifying why specific transactions were flagged.

BSA/AML and Credit Risk Applications

In BSA/AML programs, AI is being applied to:

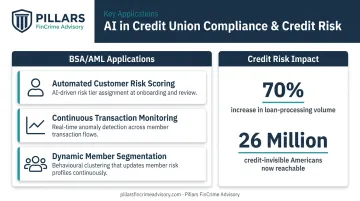

- Automated customer risk scoring — replacing manual periodic reviews with dynamic risk profiles that update as member behavior changes

- Continuous transaction monitoring — adjusting to emerging typologies rather than waiting for rule updates

- Dynamic member segmentation — grouping members by behavioral patterns rather than static demographics

On the credit risk side, machine learning models can incorporate non-traditional data points — utility payments, rental history, transaction behavior — to generate credit scores for members who would otherwise be invisible to conventional models. The Federal Reserve has noted that approximately 26 million Americans are credit-invisible, with another 19.4 million lacking sufficient recent data for a traditional score. AI-powered underwriting can serve those members.

One benchmark: FORUM Credit Union reported a 70% increase in loan-processing volume after implementing AI-enabled underwriting automation.

That opportunity carries a compliance obligation. The CFPB has been explicit that using AI or machine learning in credit decisions does not relieve creditors of the obligation to provide specific, accurate adverse-action reasons under ECOA and Regulation B. Black-box model outputs don't satisfy the requirement for genuine, specific explanation.

Fraud Detection and Operational Efficiency

AI-powered fraud detection has moved beyond transaction pattern analysis. Current applications include:

- Behavioral biometrics — detecting anomalies in how members interact with digital banking channels

- Deepfake detection — FinCEN issued Alert FIN-2024-Alert004 on November 13, 2024, specifically warning that criminals are using generative AI to create deepfake media designed to bypass CIP and CDD controls

- Real-time anomaly detection — flagging suspicious activity before transactions complete, without adding friction for legitimate members

For smaller credit unions with limited compliance staff, the operational efficiency argument for AI is especially compelling. AI-assisted alert triage and case prioritization can sharply cut the volume of manual review work, allowing compliance staff to focus on investigations that actually warrant human judgment.

Human oversight remains essential, though. Automated systems surface candidates for review — they don't replace the SAR filing decision.

The Four Risk Categories Credit Unions Face When Adopting AI

AI adoption risk isn't a single problem. Credit union leadership must account for four interconnected categories — and these apply whether AI is being used offensively (loan decisioning, automated member services) or defensively (fraud detection, cybersecurity).

Financial Risk

The cost of AI is real and often underestimated. Integration, training data preparation, ongoing maintenance, and vendor contracts can add up quickly. More critically, if an AI system produces flawed outputs — erroneous loan denials that drive away qualified members, or missed fraud flags that result in losses — the downstream financial exposure can easily exceed whatever efficiency gains were projected.

Before committing to an AI platform, credit unions should conduct an explicit ROI evaluation that accounts for:

- Direct costs: licensing, integration, training, ongoing maintenance

- Indirect costs: staff retraining, compliance review of model outputs, vendor oversight burden

- Downside scenarios: what happens if the model fails, drifts, or is taken offline

Reputational Risk

Bias in AI models — particularly in lending or member risk scoring — can produce discriminatory outcomes even when no discriminatory intent exists. ECOA and the Fair Housing Act apply regardless of whether a human or an algorithm made the decision. A public enforcement action tied to AI lending bias creates member trust damage that's difficult to reverse.

The joint enforcement statement signed by the CFPB, FTC, DOJ, and EEOC in April 2023 made this explicit: automated systems are not a legal defense for discriminatory outcomes. Credit unions deploying AI in any member-facing decision must validate models for disparate impact and document that validation.

Operational Risk

Three operational risks deserve attention:

- Vendor concentration — over-reliance on a single AI provider for critical functions creates systemic exposure if that vendor experiences an outage, is acquired, or modifies its model without notice

- Model drift — AI accuracy degrades as member behavior evolves; a model that performed well at deployment may silently produce worse results 18 months later without triggering any alerts. Ongoing outcomes monitoring and periodic model review are the only reliable defenses

- Legacy system integration — connecting AI tools to legacy core banking systems introduces new failure points that must be addressed in business continuity and disaster recovery planning

Legal and Regulatory Risk

The NCUA has not issued AI-specific regulations. But that doesn't create a gap — existing technology-neutral regulations cover AI use fully. Information security standards, BSA/AML obligations, fair lending requirements, and data privacy laws all govern how AI can be deployed.

The regulatory landscape is moving fast. Recent signals from federal regulators make clear that AI governance expectations are actively taking shape:

- FinCEN's deepfake alert — flagged AI-generated identity fraud as an emerging BSA/AML threat

- Treasury's December 2024 report — outlined AI risk management expectations for financial services firms

- CFPB's adverse-action circulars — reinforced that explainability requirements apply to algorithmic credit decisions

Credit unions must monitor this space continuously, not just at exam time.

NCUA and Regulatory Expectations for AI in Credit Unions

The NCUA's Current Supervisory Posture

The NCUA has stated clearly that it supports AI adoption when implemented safely, soundly, and in compliance with existing law. Examiners evaluate AI tools within the standard supervisory framework — safety and soundness, internal controls, ongoing monitoring, and compliance with applicable regulations. AI is not treated as categorically different from other innovative technology.

What the NCUA has also made explicit: credit unions must identify risks unique to AI and implement appropriate controls — and that's not a light standard to meet.

Model Risk Management Expectations

Credit union examiners now reference SR 11-7 — the Federal Reserve and OCC's foundational model risk management guidance — as a benchmark for AI governance expectations. Under this framework, credit unions must:

- Document how AI models function and what they are designed to do

- Validate model accuracy and fairness at deployment

- Monitor for drift, bias, and performance degradation on an ongoing basis

- Maintain a model inventory that captures all models in use, their purpose, and their validation status

This is an ongoing operational responsibility — one that requires dedicated resources, documented processes, and consistent examiner-ready evidence.

Third-Party AI Vendor Oversight

NCUA Letters to Credit Unions 07-CU-13 and 01-CU-20 apply directly to AI vendors. Credit unions must understand how vendor AI products function, what risks they introduce, and whether the vendor's controls are adequate. Board and management accountability for vendor AI performance is explicitly expected — "we used a vendor" is not a sufficient answer to an examiner's question about model governance.

Treasury, FinCEN, and Emerging Typologies

FinCEN's 2024 deepfake alert has direct implications for SAR filing and CIP procedures. Institutions should:

- Add deepfake red flags to fraud monitoring protocols

- Update SAR narratives to include the keyword "FIN-2024-DEEPFAKEFRAUD" when filing on suspected deepfake-related activity

- Review CIP procedures to assess whether current identity verification methods can detect AI-generated synthetic identities

FinCEN's 2024 identity-related suspicious activity report found 2.4 million identity-related BSA reports in 2021, totaling $351 billion, with impersonation accounting for 69% of reports. The data makes one thing clear: AI-enabled identity fraud is already present at scale across the BSA reporting ecosystem.

Building an AI Risk Governance Framework

Foundational Governance Elements

An effective AI governance structure for credit unions requires:

- A cross-functional governance committee drawing from compliance, IT, risk management, and business leadership — not siloed within IT

- A documented AI use case inventory that captures every current and planned application, its purpose, and its risk classification

- A board-approved AI risk appetite statement defining which use cases the institution will pursue and at what tolerance level

The FSB's 2026 consultation on responsible AI adoption explicitly calls for institutions to maintain AI use case registries and align AI adoption decisions with documented risk appetite. Credit unions that build these structures now will be better positioned when examiners come asking for evidence of program maturity.

Continuous Monitoring

Model validation at deployment is necessary but not sufficient. Models must be reviewed on a defined schedule for accuracy, fairness, and regulatory alignment. Changes in member behavior, product mix, economic conditions, or regulatory expectations may all require model updates.

What triggers a review should be defined in advance. Common triggers include:

- Significant shifts in member demographics or loan volume

- New product lines or changes to underwriting criteria

- Updated regulatory guidance affecting model inputs or outputs

- Performance thresholds falling below accepted accuracy or fairness benchmarks

Deciding review criteria after a problem surfaces is too late.

Putting these governance structures in place is where frameworks stop being theoretical and start holding up under examiner scrutiny. Pillars FinCrime Advisory works with credit unions and financial institutions to build scalable, audit-ready compliance frameworks — including risk assessments and transaction monitoring program optimization — that account for the operational realities of AI adoption and position institutions to demonstrate program maturity to NCUA examiners.

Vetting AI Vendors: What Credit Union Leaders Need to Know

Due Diligence Questions That Matter

Standard vendor management checklists weren't designed for AI. Before contracting with an AI vendor, credit unions should get clear answers to:

- How does the model make decisions — and can those decisions be explained to a regulator or a member?

- What data was used to train the model, and how is member data protected during ongoing operations?

- How is model performance tracked, reported, and to whom?

- What access does the credit union retain to model documentation, validation reports, and performance data?

- Has the vendor's model been examined by a federal regulator, and what was the outcome?

Contract Provisions

AI vendor contracts require clauses that standard vendor agreements often don't include:

- Data ownership: Clarify who owns data used to train or refine the model — this is often left ambiguous in standard agreements

- Audit rights: Require explicit contractual access to model documentation and performance reporting, not just verbal assurances

- Breach notification: Establish clear timelines and procedures for notifying the credit union of a model failure or data incident

- Model change notification: Require advance notice when the vendor modifies the model's architecture or training data

- Termination rights: Specify data return, transition assistance, and business continuity provisions if the relationship ends

The OCC/FRB/FDIC interagency third-party risk guidance issued in June 2023 addresses many of these provisions directly, and credit union examiners are referencing it.

Concentration Risk

Over-reliance on a single AI vendor for critical risk assessment functions is a systemic exposure that belongs in your business continuity plan. If that vendor experiences an outage, gets acquired, or changes its model without sufficient notice, transaction monitoring coverage, fraud detection, and loan decisioning can all be compromised simultaneously.

Before that happens, build a documented response:

- Map your dependency on each AI vendor and the functions it supports

- Assess the business impact of a vendor failure or forced transition

- Maintain a contingency plan that addresses coverage gaps during any outage or migration

Frequently Asked Questions

Does the NCUA have specific AI regulations that credit unions must follow?

The NCUA has not issued AI-specific rules. Existing technology-neutral regulations — covering safety and soundness, BSA/AML compliance, fair lending, information security, and third-party oversight — apply fully to AI systems. Examiners evaluate AI within the standard supervisory framework and expect credit unions to identify and control risks unique to AI.

How can credit unions ensure AI-driven lending decisions comply with fair lending laws?

Credit unions must validate AI credit models for potential disparate impact, document model logic and data inputs, and conduct regular fair lending reviews. ECOA and the Fair Housing Act apply regardless of whether a human or an algorithm made the decision. The CFPB also requires specific, accurate adverse-action explanations for complex AI models.

What is model risk management and why does it matter for AI?

Model risk is the risk of adverse outcomes from reliance on inaccurate or misused models, including financial loss, reporting errors, and compliance failures. AI models require ongoing validation, documentation, and monitoring to ensure accuracy and appropriate use — this is a continuous operational responsibility, not a one-time compliance check.

How does AI improve BSA/AML compliance for credit unions?

AI improves transaction monitoring by reducing false positives, enabling dynamic member risk scoring, and detecting emerging typologies faster than static rules. Human oversight and SAR filing judgment remain essential — compliance staff must evaluate and act on what AI surfaces, not just accept its output.

What should credit unions look for when evaluating AI vendors for risk assessment?

Focus on five areas: model explainability, data security and privacy protections, audit rights embedded in the contract, ongoing performance reporting cadence, and the vendor's track record under regulatory examination. Vendors who can't answer these questions clearly will create examination problems down the road.

How do credit unions balance AI innovation with NCUA examination readiness?

Examination readiness requires documented governance policies, a current AI use case inventory, evidence of ongoing model monitoring, and clear board-level accountability for AI risk. Proactive documentation of how each AI tool is governed — not just deployed — demonstrates the program maturity examiners are looking for.